Abandoned oil and gas wells make for good news stories: Wildlife Habitat Threatened by Oil Leaking from Old Well; Agency Plugged 300 of 35,000 Orphaned Wells This Year. These wells, many of them drilled in the first decades of America’s oil-drilling era and now orphaned by their operators, can each cost local governments tens of thousands of dollars to clean up. If they are not properly decommissioned, they may contaminate groundwater or leak methane.

However, in our new RFF report, coauthored with RFF’s Jhih-Shyang Shih and Clayton Munnings, we argue that the scope of the wells deserving concern should be expanded to include all inactive wells—any wells that have not produced oil or gas for a meaningful period of time (typically thirty days or more). All inactive wells carry environmental (and financial) risk.

Today’s regulators and industry engineers have fixed part of the legacy problem of older wells. Oil and gas agencies maintain digital inventories of all wells drilled. Wells are constructed with several layers of steel casing and cement. Wells that have stopped producing are plugged with a combination of clay, cement, and mechanical plugs. And regulations require operators to provide a bond to guarantee proper decommissioning of their wells, which is returned only after the operator has satisfactorily completed the process.

So why do state agencies still see increases in the number of orphaned wells, particularly during industry downturns? And if bonds are supposed to help cover the cost of decommissioning, why do states still require money from legislative appropriations, industry fees, and environmental cleanup funds to deal with these orphaned wells year after year?

A year ago, we launched a research effort to answer these questions and identify ways in which inactive well regulations could ensure that operators—rather than the state or the public—would bear the environmental and financial risks. We examined the inactive well regulations and financial incentives facing well operators with the help of representatives from state oil and gas agencies, scholars in the field, and industry consultants. We asked about the environmental risks posed by these wells, the costs to decommission a well, the size of the bond that operators are required to post, and the regulations imposed on operators when their wells stop producing.

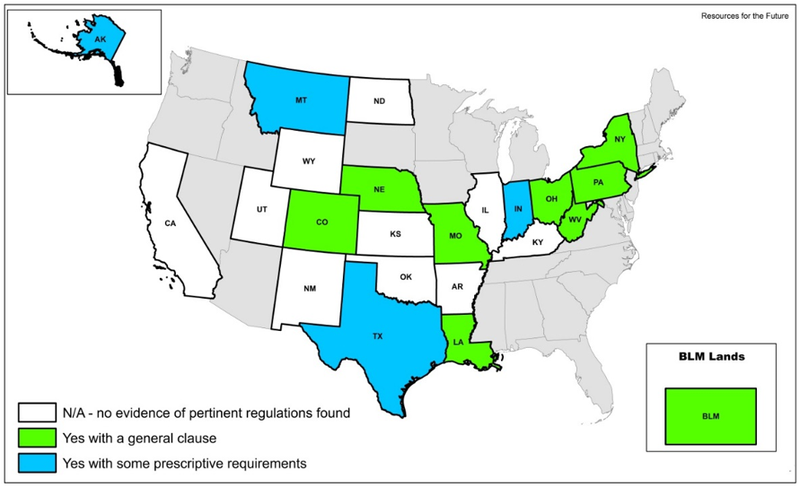

Understanding the last two issues involved thoroughly reviewing the regulations governing inactive wells in 22 states and on federal lands managed by the Bureau of Land Management. (This follows on prior RFF research that reviewed state shale gas regulations.)

Our report identifies a number of reasons why inactive wells don’t always get decommissioned properly (some of these have been articulated elsewhere, in the grey literature, popular press, and peer-reviewed literature):

- Promising to decommission a well is cheap; keeping that promise isn’t. When we compared average bond amounts to average decommissioning costs in 12 states, costs exceeded bonds in 10 of them. As a result, it is in an operator’s interest to maintain his or her wells in a state of temporary abandonment instead of incurring the cost of decommissioning.

- Some wells requiring decommissioning may be masquerading as “temporarily abandoned” wells. Operators may file for temporary abandonment if they can prove that their wells have the potential for future use; yet, an audit of Louisiana’s Office of Conservation in 2014 found that 46.5 percent of the wells in “future utility status” had been in that status for more than 10 years. Our regulatory review revealed that only five states stipulate a duration beyond which a well’s temporary abandonment status can no longer be extended (see full report), while only 12 require operators to credibly demonstrate that their wells have future utility (see map).

Map. Presence of a Requirement for Operators to Show Future Usefulness of Temporarily Abandoned Wells

- Wells are sometimes transferred to operators that lack the financial means to decommission them, or that are at risk of becoming bankrupt particularly during industry downturns. This is an industry in which wells frequently change hands from industry giants to mom-and-pop operators and, at present, buyers are merely required to cover the cost of the bond attached to the well, which provides no guarantee that they’ll be able to cough up the money required for decommissioning.

In our report, we recommend the following to help address these issues:

- Bond amounts should be compared to and revised to match decommissioning costs in each state. These bonds must be calibrated to account for a variety of factors influencing cost (e.g., well depth);

- Some states should tighten their requirements for a well to remain in temporary abandonment status (e.g., by mandating that an operator demonstrate the future economic viability of a well); and

- States should ensure that an operator purchasing a well is financially stable, and/or hold the original owner of a well liable for decommissioning it even after ownership is transferred.

Other recommendations are discussed in the report’s Summary of Key Findings.

Of course, there is always more to be learned. To better understand the nature of the problem, it’d be nice to know how likely it is that a well will leak even after it’s been permanently decommissioned (we’ve heard anecdotal evidence suggesting this), how often operators choose to post blanket bonds (a quantity discount for operators with large populations of wells in a single state), and how effectively the regulations we reviewed are enforced in practice. In addition, identifying why some states have been more effective at monitoring inactive wells and how they’ve been able to introduce ambitious solutions—such as increasing bonding requirements—could be helpful to all states facing this challenge.

The authors would like to thank the Paul G. Allen Family Foundation for funding this project.