The American taxpayer helps underwrite oil, gas, and coal production with very little to show for it. The businesses drilling for oil and gas and mining coal enjoy effectively lower income tax rates than other American businesses because of an array of favorable provisions in the US tax code. These so-called tax expenditures—which are effectively equivalent to government spending—subsidize oil, gas, and coal companies by about $4.9 billion annually. In return, however, there is virtually no change in US production.

In 2009, President Obama pledged to eliminate these provisions as part of an agreement among the G20 nations to phase out fossil fuel subsidies. In every budget proposal since taking office, the administration has called for eliminating these subsidies—but with no success in Congress. In his fiscal year 2015 budget released in March, the president again proposed to strike fossil fuel subsidies from the tax code. And in February, Republican Congressman Dave Camp, the chairman of the House Ways and Means Committee, introduced a comprehensive tax reform proposal that would eliminate some of these subsidies.

Proponents of fossil fuel subsidies claim that eliminating them would reduce US oil and gas production and cost American jobs. But analyses show very small declines in production that would be easily dominated by the current trend in increasing oil and gas production as a result of technological innovation. So what's really at stake?

Tax Provisions that Subsidize Oil, Gas, and Coal

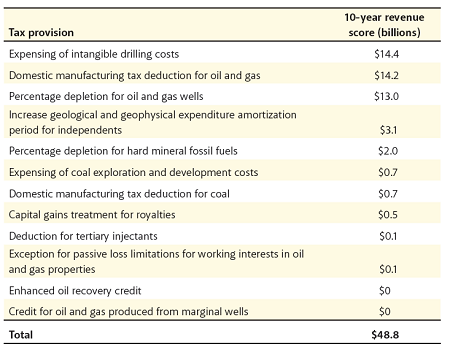

From as far back as 1913—the year a constitutional amendment legalized the income tax—fossil fuel extraction companies have received tax breaks that subsidize their activities. Most of these tax code provisions lower the cost of investing in oil, gas, and coal development projects, and they all lower in a preferential manner the corporate tax rate on a specific source of income—in other words, picking winners through the tax code. The three largest tax expenditures—the expensing of intangible drilling costs, the domestic manufacturing tax deduction for oil and gas, and percentage depletion for oil and gas wells—represent nearly 90 percent of the $4.9 billion in annual subsidies (Table 1).

Table 1. Provisions of the US Tax Code that Subsidize Fossil Fuel Extraction

Notes: The last two provisions in this table are not expected to have a revenue impact because they phase out at oil prices below the levels expected over the 10-year scoring window. Source: Office of Management and Budget, FY2015 Administration Budget

The eligibility for and generosity of these programs differ between integrated companies—those that produce and refine oil and market petroleum products—and independent companies, those that only operate upstream in the extraction of oil and gas. Supermajors, such as ExxonMobil, BP, Chevron, and Royal Dutch Shell, that extract, refine, and retail oil can claim fewer subsidies per barrel of oil extraction than independent (and especially small independent) oil companies.

In the US tax code, a firm investing in a capital project—say a new factory or office computers—typically depreciates the investment costs over the useful life of the capital. In contrast, oil and gas firms expense all or most of their drilling-related expenditures that do not have salvage value, referred to as intangible drilling costs. These typically include geological surveying, wages, fuel, repairs, and supplies associated with well development. As a result, the provision effectively lowers the tax rate on income from such projects relative to capital investments elsewhere in the economy, distorting investment decisions. This has led to inefficiently low investment outside of the oil and gas sector and inefficiently high investment within it.

The provision specifically allows independent oil companies to expense all their intangible drilling costs, whereas integrated oil companies can expense up to 70 percent of these costs and must depreciate the balance over five years. This skews investment in oil and gas development away from integrated oil firms and toward independent oil companies, although there is no public policy rationale for doing so.

The percentage depletion tax provision also disproportionately benefits smaller firms. The oil and gas firms producing less than 1,000 barrels per day may deduct a percentage of their revenues, yet firms with larger volumes must deduct the capital cost of the wells. Indeed, with high oil prices, small firms may be able to claim deductions through percentage depletion over the life of a well that significantly exceed the capital cost of the well. In contrast to some oil tax expenditures that phase out with higher oil prices, such as the credit for enhanced oil recovery projects, the effective subsidy from percentage depletion increases as oil prices rise. This also lowers the effective tax rate on these projects and skews investment away from non–oil and gas capital projects and oil and gas development by larger and integrated firms.

In 2002, a World Trade Organization (WTO) ruling found that US tax law effectively subsidized manufacturing exports and thus violated the international agreement regarding trade and subsidies. As a result, Congress struck the WTO-illegal tax provision and replaced it with a domestic manufacturing tax deduction. While oil and gas development is not part of the manufacturing sector nor was the United States a meaningful exporter of either oil or gas at the time, Congress determined that these activities also could claim the manufacturing tax deduction. This provision permits oil and gas producers to claim a 6 percent deduction, and a related provision allows coal producers to claim a 9 percent deduction of taxable income. Like the other subsidies, this provision provides a lower rate on a favored source of income.

Of course, subsidies are not by definition bad public policy. For example, subsidizing investment in low- or zero-pollution energy sources can deliver important environmental and health benefits, especially in the absence of carbon and other pollution pricing. Some subsidies may target novel technologies and facilitate innovative activity. For example, the now-expired unconventional natural gas production tax credit provided support for nascent shale gas exploration technologies in the 1980s and 1990s.

The subsidies listed in Table 1, however, do not focus on innovative or pollution-reducing activities. They indiscriminately lower the cost of investing in another oil and gas field or another coal seam. As a result, they distort and subsequently lower the return on investment across the US economy. In addition, by reducing tax revenues from resource extraction, these subsidies must be effectively financed by taxes elsewhere in the economy, which may further reduce non–fossil fuel investment.

Impacts of Eliminating Subsidies for US Oil and Gas Production

Oil and gas tax expenditures do not have a meaningful impact on US oil and gas production. Oil and gas companies have had access to two of the most prominent subsidies, the intangible drilling cost and percentage depletion provisions, since long before the first oil shock in 1973. Over the 1973–2008 period, US oil production declined each year an average of more than 120,000 barrels per day. Since 2008, US oil production has averaged an annual increase of more than 350,000 barrels per day. These subsidies could not reverse the decline in domestic production before 2008, and high oil prices and technological innovation, not subsidies, explain the rapid production growth in recent years.

The remarkable technological innovation that has transformed the US oil and gas sector over the past half dozen years more than offsets any adverse impacts that subsidy elimination would have on domestic production. The National Research Council (NRC) recently modeled the elimination of the percentage depletion provision for natural gas. For this analysis, the NRC used the US Department of Energy's (DOE's) 2011 benchmark energy forecast through 2035. Over the 2010–2035 period, the NRC estimated that eliminating this subsidy would reduce US gas production by about 2 percent relative to this 2011 forecast.

This impact appears modest on two dimensions. First, the NRC estimates that US gas production would continue to increase in the years immediately after subsidy elimination and remain above 2010 levels every year through 2035. Thus, the impact is not a fall in the level of production, but slower growth in production.

Second, and more profoundly, the DOE's 2013 version of the benchmark forecast shows 15 percent greater gas production through 2035 than the 2011 version used by the NRC. Continuing innovation has led the DOE, year after year, to raise its forecast domestic production and lower its estimated wellhead prices.

RFF Visiting Fellow Stephen Brown evaluated the elimination of oil and gas tax expenditures with his colleague Maura Allaire in 2009. He found that US oil production would be about 26,000 barrels per day lower than it would be without the subsidy elimination. Also in 2009, the US Department of the Treasury estimated a similarly modest impact on domestic oil production on the order of about 0.5 percent. The recent, dramatic increase in US oil production—reaching levels unseen since the 1980s—puts this production impact into context. Since January 2009, the average monthly increase in domestic oil production is about 45,000 barrels per day. Thus, it takes about 17 days to make up for a decline of 26,000 barrels per day of production.

If the point of these subsidies is to stimulate US production, then the taxpayer is not getting a good deal. If a private company spent nearly $5 billion per year to produce 26,000 barrels per day, it would lose a lot of money. Even applying the Department of the Treasury's 0.5 percent production impact to today's higher level of US oil production translates into the taxpayer spending several hundred dollars per barrel of incremental production. This reflects the fact that the vast majority of these subsidies go to producers that do not change their production in response to the subsidies.

Since independents finance projects substantially through cash flow, instead of raising debt, eliminating the tax provisions that subsidize their activities could impact their financing strategy. For example, these companies may need to raise debt and equity for their drilling projects, not unlike how firms in other sectors of the economy finance major projects. In other words, eliminating these subsidies requires them to operate on a level playing field for attracting investment along with supermajors and other companies throughout the economy.

Environmental Impact of Eliminating Fossil Fuel Subsidies

These subsidies' very small production impacts result in imperceptible effects on US fossil fuel prices and subsequent domestic consumption. As a result, the current subsidies in the US tax code likely have little direct impact on US carbon dioxide emissions. Nonetheless, eliminating these subsidies could lead to significant carbon dioxide emissions reductions globally.

Given the US effort in securing the G20 agreement to eliminate fossil fuel subsidies in 2009, the failure to make any domestic progress hamstrings US officials in leveraging progress by other G20 nations. While this issue continues to receive attention from leaders in G20 summits, the progress to date has been slow. Eliminating these domestic subsidies would empower the United States to push other large economies to do likewise.

Eliminating fossil fuel subsidies around the world would deliver quite dramatic carbon pollution benefits, as well as important economic and fiscal impacts. The International Energy Agency estimates that eliminating fossil fuel consumption subsidies, currently about a half trillion dollars annually, would reduce carbon dioxide emissions by about 7 percent by the end of the decade and 10 percent by 2050. Doing so would also free up resources—amounting to at least a quarter of some countries' government budgets—that could be used to address important social needs, such as public health and education.

Political Implications

Political opposition to subsidy reform has effectively stifled any meaningful congressional debate on this issue. The best prospects for eliminating these subsidies may lie in comprehensive tax reform. Indeed, the recent proposal by Congressman Camp eliminates percentage depletion and the manufacturing tax deduction, as well as some of the smaller fossil fuel tax expenditures, as part of a tax reform that also lowers the corporate income tax rate. While political prognosticators are not optimistic about a serious debate on tax reform this year, this proposal does illustrate that eliminating oil, gas, and coal tax expenditures as part of a larger reform could be politically appealing.

Further Reading

Aldy, Joseph E. 2013. Eliminating Fossil Fuel Subsidies. In 15 Ways to Rethink the Federal Budget, edited by Michael Greenstone, Max Harris, Karen Li, Adam Looney, and Jeremy Patashnik. Washington, DC: The Hamilton Project, Brookings.

Allaire, Maura, and Stephen Brown. 2009. Eliminating Subsidies for Fossil Fuel Production: Implications for US Oil and Natural Gas Markets. Issue brief 09-10. Washington, DC: RFF.

National Academy of Sciences. 2013. Effects of US Tax Policy on Greenhouse Gas Emissions. Washington, DC: National Academies Press.

A version of this article appeared in print in the Spring/Summer 2014 issue of Resources magazine.