Onshoring the Mineral Supply Chain: Structural Constraints, Policy Tools, and Research Gaps

This report examines the economic, technical, workforce, infrastructure, and policy challenges of strengthening the US critical minerals supply chain and proposes strategies to prioritize investments and improve supply resilience.

Abstract

Critical minerals, such as lithium, nickel, graphite, and rare earth elements, are vital components of defense, energy, and transportation technologies. As demand for these technologies and their minerals grows, the geographic reality of where they are extracted, processed, and manufactured has drawn increasing attention. Though the United States has some mineral reserves and strategic industrial policies for certain base metals, its participation in the mineral supply chain has declined over the past century, and market concentration in foreign supply has increased concerns about exposure to supply disruptions.

In response, recent administrations have established priorities around critical minerals and taken steps to mitigate supply risk, with the current administration taking a much more active role in advancing its critical minerals policy goals, including unprecedented investments in individual critical mineral mining and refining projects.

We present new data that highlight the market and economic challenges to onshoring the critical mineral supply chain, noting the large technical, geographic, and economic differences across minerals. We then discuss workforce, infrastructure, and social license challenges to increasing domestic production, along with the various federal efforts to ensure secure access to mineral supply. Finally, we present a framework for how investments can be prioritized to maximize the efficacy of federal expenditures and reduce supply risk and how policies can be evaluated in their support of these efforts. We conclude by identifying research gaps and proposing directions for future work to support evidence based industrial policy and improve the resilience, competitiveness, and social legitimacy of the federal critical minerals strategy.

1. Introduction

Critical minerals, such as lithium, nickel, graphite, and rare earth elements (REEs), are the material foundations of defense technologies and energy infrastructure. As domestic demand for these technologies and their minerals grows, the geographic distribution of critical mineral extraction, processing, and manufacturing has emerged as a central policy concern, particularly in cases with high geographic concentration in production. The United States is a net importer across critical mineral supply chains: it extracts minimal quantities, processes almost nothing, and produces very few downstream products (magnets and batteries) (Spiller et al. 2023).

Although the United States has mineral reserves, its participation in the mineral supply chain has declined over the past century, as lower-cost options emerged overseas. Large Chinese investments in extraction and processing capacity, in particular, have reduced import costs and the incentives for domestic investment. However, rising geopolitical tensions over the last few decades have increased concerns about reliance on foreign supply and exposure to supply disruptions.

In response, prior presidential administrations have established priorities around critical minerals and taken steps to mitigate supply risk, often by strengthening trade relations with allied nations (“friendshoring”). Over the past decade, critical mineral policy has also increasingly been tied to industrial policy, as administrations have sought to leverage rising mineral demand to ramp up domestic manufacturing.

The Trump administration has taken a much more active approach, including an unprecedented slew of direct equity investments in individual mining and refining projects. Though domestic critical mineral production remains a priority, as under the previous administrations, multilateral discussions around trade agreements and price floors with allied nations have intensified.

Although geopolitical dynamics have clearly motivated US policy action, they do not by themselves define a single objective for it. In practice, critical minerals policy has been expected to advance multiple objectives: (1) supply chain resilience, by reducing exposure to disruptions and concentrated foreign supply; (2) industrial policy, by increasing jobs and expanding domestic capacity in extraction, processing, and manufacturing; and (3) competitiveness, by ensuring that US firms can compete globally in minerals markets.

These objectives are not always aligned. Strategies that prioritize resilience in the near term may emphasize diversification across allied supply chains rather than domestic build-out, particularly where global capacity is already established and cost-advantaged. Conversely, efforts to expand domestic production may require significant subsidies due to high domestic costs, reducing the ability to achieve long-term global competitiveness. Thus, policies aimed at achieving one goal may inadvertently reduce the country’s ability to achieve the others.

We highlight the challenges to onshoring this supply chain, noting the technical, geographic, and economic differences across minerals along with fundamental themes that can serve as criteria or objectives for any national policymaking. We conducted a literature review and collected data from technical reports, proprietary datasets on firm-level costs, and open-source information on asset-level ownership. We also conducted 18 structured interviews with experts with a range of policy, research, industry, and academic backgrounds, during which we asked about their views on (1) the barriers to onshoring the supply chain; (2) federal policy actions—past, present, and prospective; and (3) important research directions that can help guide policy. These interviews informed our analysis, and we thank participants for their time and input.

1.1. A Brief Overview of Critical Minerals in the United States

During the gold rush of the mid-19th century, mining became a major industry in the United States. The General Mining Act of 1872, See https://www.govinfo.gov/app/details/COMPS-5337. enacted in response to that mining boom, remains in effect and serves as the foundation for domestic mining policy. Before stronger environmental and labor policies emerged in the 1970s, the mining industry created substantial environmental and social damages, particularly from failed or abandoned projects (US GAO 2023).

Mining and minerals processing are highly capital-intensive industries, and global market liberalization opened US producers to competitors with structurally lower costs. Domestic environmental and labor standards introduced safeguards for domestic mining and major industrial projects, attracting investments to countries with more permissive regulation (though the scale of this effect is debated; e.g., see Gill et al. [2018]). Over time, the US share of domestic production declined with the accompanying loss of labor capacity and expertise.

As the interest in onshoring grows (discussed in Section 1.4), questions are emerging about the feasibility of expanding domestic supply chains, given the limited domestic reserves of certain minerals and the high capital costs of investing in new mines and processing plants. Many important new energy and defense minerals are not mined and processed in the United States in meaningful quantities, except for copper, lithium and certain rare earths. However, many critical minerals are by-products (or found in the waste streams) of other mining operations. Recovering these could help meet the growing demand but extraction may not be economically viable, and more geoeconomic research and technical studies are required to understand the resource base.

1.2. Geopolitics

The supply chains of many critical minerals are geographically concentrated in a few countries. At the extraction stage, cobalt, natural graphite, and REEs are highly concentrated, with one or two countries accounting for over 70 percent of global supply (IEA 2021). Cobalt extraction is dominated by the Democratic Republic of Congo (DRC) and natural graphite extraction and rare earth minerals processing by China. In addition to a comparative advantage in certain primary extraction and processing capacities, China has invested in extraction companies worldwide, allowing it to have large ownership stakes. For example, in 2020, it owned or held financial stakes in 15 of the 19 producing cobalt firms in the DRC (Lipton and Searcey 2022).

The most significant geographic concentration is in the processing phase, with China responsible for processing most of the enabling critical minerals and engineered metals for defense and new energy technologies. As a result, even if minerals are extracted in the United States or an allied country, such as Argentina or Australia, they are generally sent to China for processing before being supplied to a battery components manufacturer elsewhere. This dynamic is exemplified by the lithium-ion battery supply chain—even though extraction is geographically diversified, the remainder of the supply chain is concentrated in China, creating the (perceived) risk of supply disruptions. Indeed, China previously implemented some mineral export bans for strategic defense and energy supply chains, though they were predominantly short lived and likely used as negotiation tactics (Nguemgaing et al. 2025).

If the United States seeks to create domestic critical minerals supply chains, it would need to compete with this low-cost, global alternative that is already built out and operational. Doing so would require building mines, processing plants, and manufacturing plants and investing in innovation and research and development to reduce costs, increase technical knowledge, and advance technological development. Such a build-out could take decades, cost many billions of dollars, and require significant collaboration across local, state, and federal governments.

The question, then, is whether the United States can advance certain parts of the supply chain effectively and quickly enough to justify the associated costs and address the risks, while also achieving other policy goals (e.g., industrial policy). As we seek to demonstrate, domestic industrial policy goals and market diversification may not be complementary objectives.

1.3. Beyond Geopolitics: What Is Needed to Support the Domestic Supply Chain?

Beyond geopolitics, a key question is whether the United States can actually build a competitive, resilient, and durable critical minerals industry. That requires first understanding the constraints the industry faces.

To effectively develop the domestic supply chain envisioned by recent policies, companies must establish new mining, processing, and refining operations. This requires economic feasibility and some degree of confidence that investments will result in profits. However, several challenges contribute to uncertainty for companies and dissuade further investment. We examine key challenges that limit this build-out, including limited economic project viability, midstream gaps and demand uncertainty, lack of workforce and technical know-how, and timeline challenges and need for community buy-in.

Having understood the constraints the industry faces, it is important to assess the role that policies can play in helping overcome these challenges. Policies can be assessed along multiple dimensions, beginning with the extent to which they advance the various objectives that often motivate critical minerals policy: (1) supply-chain resilience, (2) the economic competitiveness of downstream industries, and (3) industrial policy goals. Second, they can be evaluated based on the fiscal costs and risks each instrument imposes on the public sector. Third, they can be assessed based on who bears the costs—including taxpayers, consumers, and firms—and the distribution of environmental burdens across communities and jurisdictions. Finally, they can be assessed based on policy durability, recognizing that investment decisions in mining, processing, and manufacturing depend on the credibility and longevity of policy commitments over multiyear timelines. We apply this framework when discussing the policies leveraged by the government within the minerals sector. We then analyze and discuss potential policy reforms that could reduce risk and improve investment certainty. Finally, we identify economic research gaps that could illuminate other potential pathways toward building out a domestic supply chain.

1.4. Evolution of Policy: Onshoring Objectives and Industrial Policy

A major inflection point in US policy response in the critical minerals sector occurred in 2010, when China banned REE exports to Japan (Evenett and Fritz 2023). This incident, though brief, highlighted the geographic concentration of resources outside the United States and potential for supply shocks, particularly given the limited US participation in the supply chain.

In 2015, the Obama administration passed the Fixing America’s Surface Transportation (FAST-41) legislation, which aimed to reduce approval times for permitting domestic mining projects by creating a federal permitting council and dispute resolution mechanisms, coordinating across permitting agencies, and increasing transparency. However, very few critical mineral mines used this process until 2025; as of writing this report, 15 mines are identified as Covered Projects and 36 as Transparency Projects under the program See https://www.permits.performance.gov/projects/fast-41-covered for a list of the Fast-41 Covered and Transparency Projects. (Permitting Council 2025).

In 2017, the Trump administration issued Executive Order 13817, directing the Department of the Interior (DOI) to develop a list of critical minerals and launched several policies reframing the sector as a matter of national security (White House 2017). Later in 2020, the administration entered into a Joint Action Plan with Canada to advance bilateral interests to secure critical minerals supply chains (Natural Resources Canada 2020), and the White House issued Executive Order 13953 (White House 2020) declaring a national emergency regarding dependence on critical minerals.

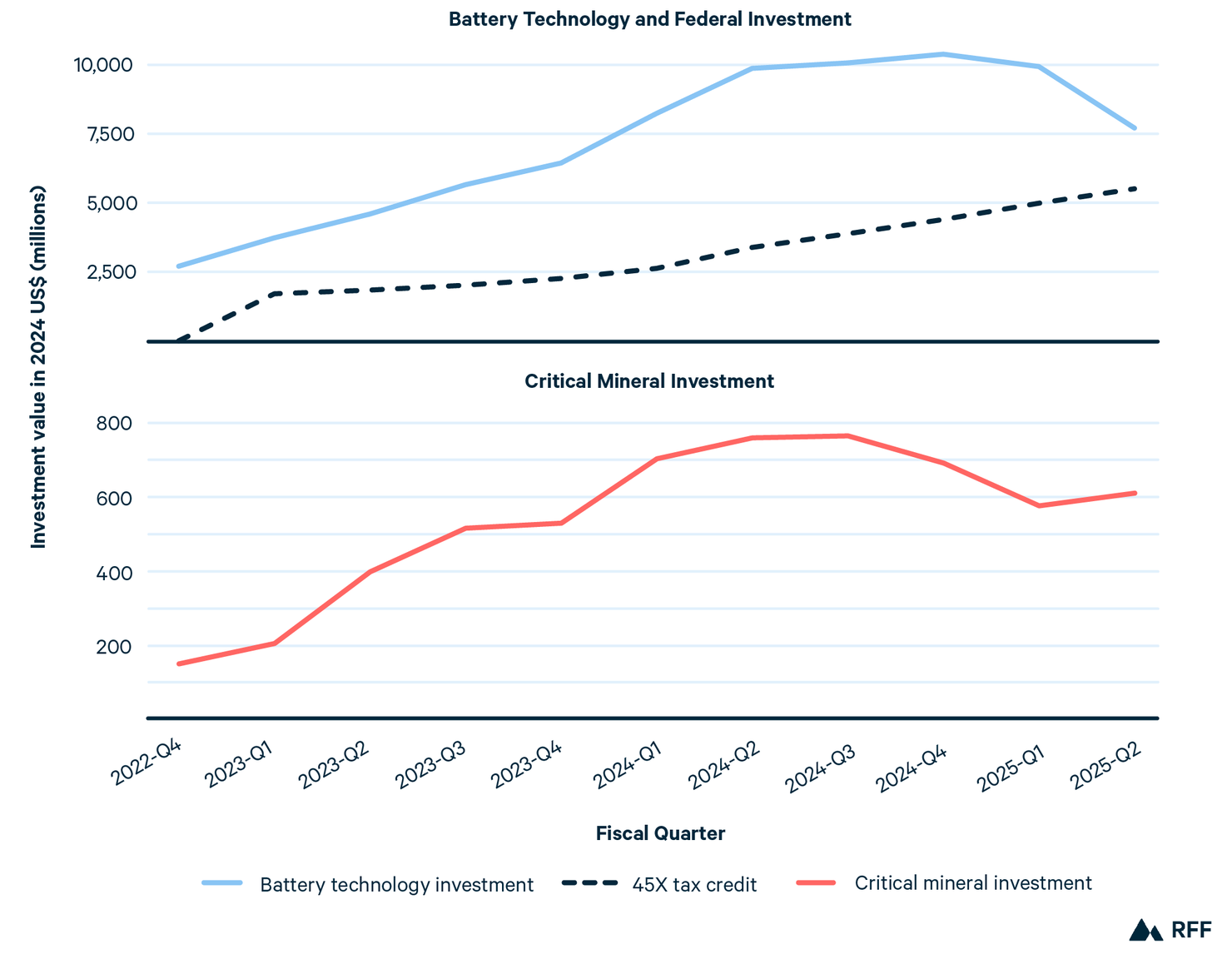

The Biden administration expanded federal policy across the full supply chain through the 2021 Infrastructure Investment and Jobs Act (IIJA) (US Congress 2021) and 2022 Inflation Reduction Act (IRA) (US Congress 2022). On the upstream part of the supply chain, the IRA provided more resources for the Bureau of Land Management and Forest Service to deal with permitting backlogs and confront understaffing. The IIJA also directed the US Geological Survey to fund an Energy and Minerals Research Facility in collaboration with the Colorado School of Mines to support energy and critical minerals research. To support the midstream portion of the supply chain, the IRA created two key tax credits: the Section 45X production credit (US Congress 2022) for critical minerals and Section 48C investment credit for advanced energy and critical mineral facilities. These incentives supported investments in mineral refining, processing plants, and battery component manufacturing.

The IIJA also supported battery production through Section 40207, authorizing grants for the support, construction, and improvement of processing facilities. Finally, the IRA focused on the demand side of the battery material issue through the Section 30D clean vehicle tax credits, which expanded prior tax credits, providing up to $7,500 in rebates for qualifying electric vehicle (EV) purchases. The primary way in which 30D tied mineral and battery supply to industrial policy goals was by conditioning eligibility on domestic or allied sourcing of minerals and battery components and restricting content from Foreign Entities of Concern (FEOCs).

The Biden administration also pursued bilateral agreements in an effort to “friendshore” critical minerals production and processing, such as the US–Japan Critical Minerals Agreement in 2023. It aimed to strengthen and diversify the supply chains for EV batteries, while also spotlighting the need to uphold strong environmental and labor standards (IEA 2025). The administration also launched the Minerals Security Partnership in 2022; the Trump administration has transformed this into its landmark Forum on Geostrategic Resource Engagement initiative (FORGE) (DOS 2022, 2026). This program is an avenue for Washington to “collaborate [with Forum nations] at the policy and project levels to advance initiatives that strengthen diversified, resilient, and secure critical minerals supply chains” (DOS 2026). However, although FORGE focuses on investing across allied nations in an effort to diversify the supply chain, it no longer emphasizes upholding environmental or labor standards as part of the agreement.

The second Trump administration shifted the approach by focusing on the upstream portion of the supply chain through several means. Executive Order 14241 on Immediate Measures to Increase American Mineral Production opened federal lands to mineral extraction; explored new financial mechanisms to support the industry, including tariffs and equity stakes (rather than Department of Defense (DOD) and Department of Energy (DOE) loans); and shortened permitting processes (White House 2025). The House passed the Critical Mineral Dominance Act in February 2025 (US Congress 2025) to codify much of this into legislation, though the Senate has yet to vote on it as of early 2026. The act aims to accelerate development through four avenues: (1) expediting the approval of permits on federal lands; (2) requiring DOI to identify and suspend or revise regulations that delay mining development; (3) measuring the economic impact of US reliance on imported mineral commodities; and (4) prioritizing geologic mapping to identify new domestic resources. Crucially, the administration phased out the IRA’s 45X and 30D provisions in the One Big Beautiful Bill Act (OBBBA), thereby removing the downstream incentives.

The Trump administration has also pursued “friendshoring” approaches through numerous bilateral deals, the expansion of US international financing mechanisms, and trading bloc approaches under development with G7 nations and, potentially, FORGE agreement partners. One example of this is the Critical Minerals Ministerial, a convening hosted by the White House in February 2026 with the goal of creating an international mineral alliance that excludes China; discussions included creating a mineral trading bloc supported by price floors. The Ministerial included 54 countries, many of which were major mineral and battery technology producers, including Australia, Canada, and Japan. Though no major multilateral agreement emerged from the meeting, the United States did sign several bilateral critical mineral frameworks and memorandums of understanding and celebrated the launch of FORGE (DOS 2026).

2. Market and Economic Challenges

2.1. Upstream Pricing and Profitability

A fundamental economic challenge in onshoring critical mineral supply chains is the capital-intensive nature of the industry and the gap between upstream costs and market prices. In this section, we examine the costs and profitability of three major battery minerals—lithium, nickel, and graphite—and REEs, using cost estimates from company-level feasibility, prefeasibility, and technical reports (see Appendix for details). We focus on these minerals due to data availability, their significant role in the EV supply chain, and their prominence in the current policy debates.

2.1.1. Lithium

Lithium can be produced through several extraction pathways, primarily from brines, hardrock deposits, and lithium-bearing clays. The former can be through either traditional evaporation or direct lithium extraction (DLE). The United States extracts lithium from brine evaporation at Silver Peak mine in Nevada. Extraction from clays and DLE are expected to become the leading sources once production begins at Thacker Pass (a clay-based lithium mine in Nevada) and in Arkansas and California (where several DLE projects are under development).

Although all commercial extraction methods can yield different lithium compounds, the processing stages vary considerably across the production pathways. Traditional brine evaporation yields lithium carbonate; DLE more readily produces either that or lithium hydroxide, both of which are used in batteries. In contrast, hardrock lithium mining produces spodumene concentrate, which needs to be further processed to create lithium hydroxide or carbonate. Nickel-manganese-cobalt batteries, which are widely deployed in EVs in the US market, require lithium hydroxide, whereas lithium-iron-phosphate (LFP) batteries, which are an increasingly adopted lower-cost alternative, can use lithium carbonate.

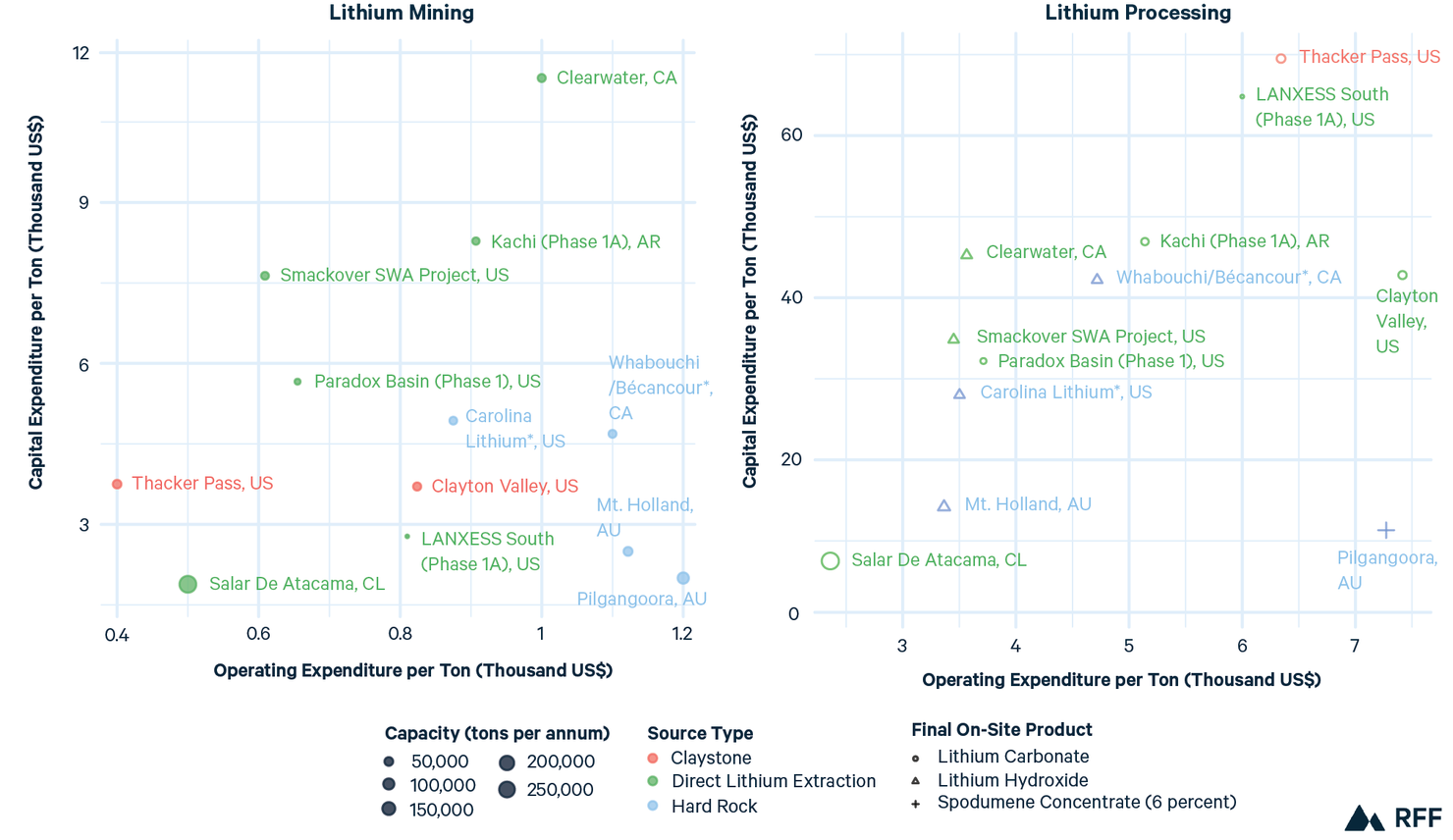

Figure 1 plots mining and processing costs for selected lithium extraction projects to allow comparison across projects. Note that cost comparisons across extraction methods are not comparable unless downstream processing costs are included. Even if the capital and/or operating costs of DLE and brine evaporation are higher than hardrock mining, spodumene (produced from hardrock mining) requires additional downstream processing, which must be accounted for. We do not include information for Silver Peak mine in the figure, given that the mine was developed in 1967, making any cost comparisons challenging at best.

Processing lithium from lithium-bearing clays is highly capital intensive and requires additional infrastructure compared to that for spodumene. This is reflected in the processing costs of Thacker Pass, which are approximately $77,000/ton compared to about $15,000/ton for Pilgangoora (Australia), a hardrock mine. The Angel Island mine is another clay-based project based in Nevada, where the lithium-bearing claystone is adjacent to a lithium brine basin. Unlike other clay-based or hardrock mines, it is expected to produce battery-grade lithium carbonate through DLE processing (according to the feasibility study). Its processing costs are significantly lower than for Thacker Pass, perhaps due to its use of DLE for processing.

Because DLE projects include both mining and processing (as opposed to hardrock mining projects, which separate the two), to cleanly distinguish the portions of costs that are associated with each, we take the following steps. For mining, we include costs associated with wellfield construction, brine extraction, and pipeline construction costs. For processing, we include costs associated with vaporization and reagent catalytic reactions.

Figure 1 highlights substantial heterogeneity in mining costs (panel a) and processing costs (panel b) in DLE projects across regions. The Smackover in Arkansas and Paradox Basin in Utah appear more competitive compared to Canadian and Argentinian projects from both capital and operating cost perspectives. However, the Salar de Atacama project in Chile is by far the most competitive in our technical report comparison (and in the lowest 15 percent in terms of C3 costs from a globally representative sample from SC Insights [2025]) for both mining and processing. Lanxess South, a tail-brine project, has low mining costs but higher processing costs. This may be partly explained by its low brine extraction costs, as it taps into the waste streams of bromine projects, thereby requiring particularly low capital expenditures for extraction infrastructure. In an interesting demonstration of geoeconomic realities, its processing costs are relatively higher because the waste brine has relatively low concentrations of lithium, requiring more reagents.

Figure 1. Lithium: Capital Expenditure Versus Operating Expenditure

DLE is a newly commercialized technology, so one can reasonably expect optimization of processes, colocation of supply-chain stages, and other efficiencies to emerge through learning-by-doing. However, some constraints remain, including limited technical expertise in processing technologies and downstream process engineering, which may increase labor costs and offset other gains. Analyses (e.g., Fitzgerald and Spiller 2025) and company feasibility studies (e.g., Jindalee Lithium Limited 2024) suggest that the long-run average market price for lithium compounds would need to be closer to $20,000/ton for most projects to be viable; 2025 lithium carbonate prices were approximately $10,000/ton. However, from July 2025 to April 2026, prices rebounded to $20,000/ton, underscoring the volatility problem in critical mineral commodity markets (SMM 2026). The majority of technical feasibility studies released in 2025 used a long-term forecast of $20,000 as the baseline for viability (SC Insights 2025).

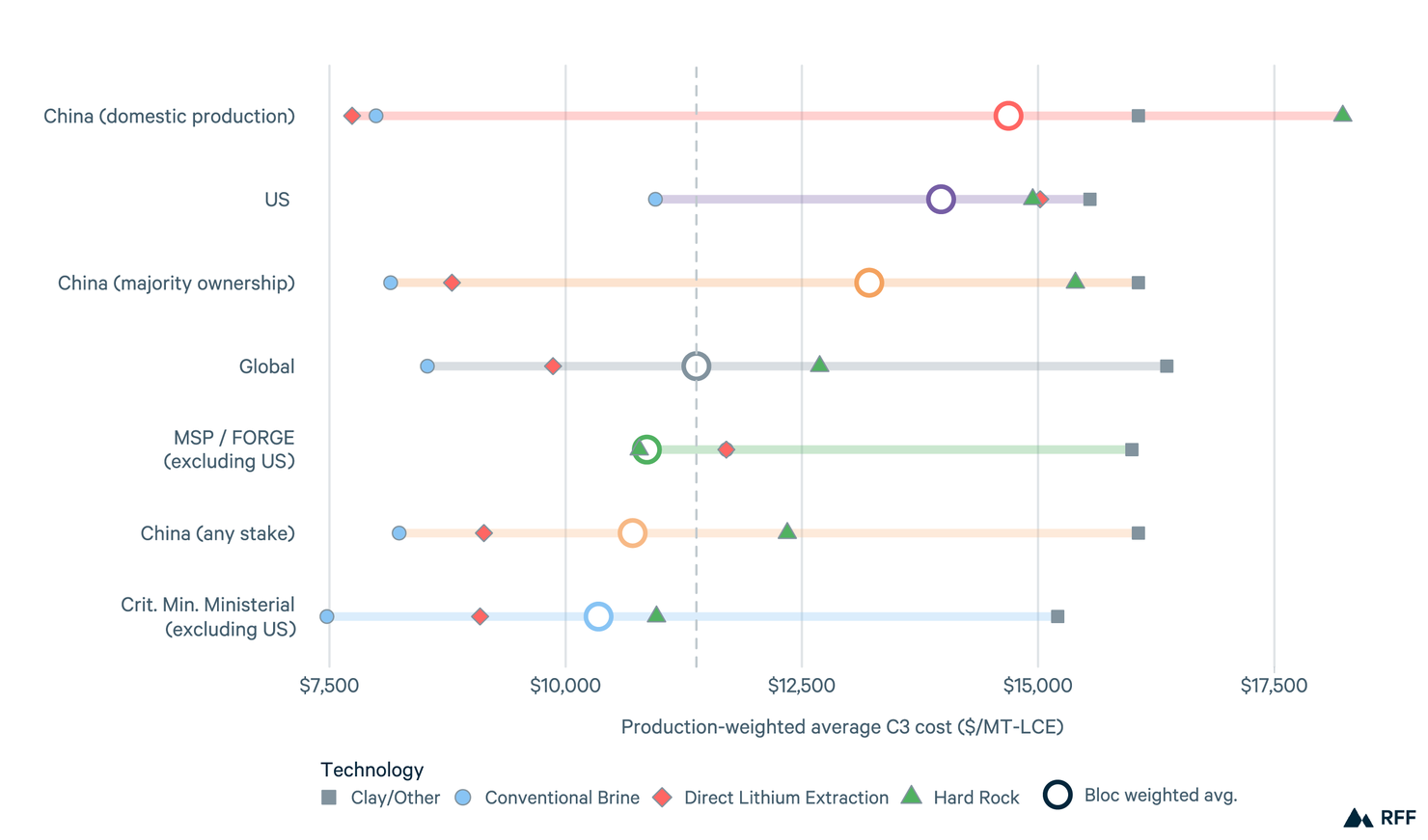

Comparing project costs across countries is challenging given differences in supply-chain integration, demand for final commodities, process technologies, and production timelines. To address this, we use aggregated data from modeled asset-level C3 costs C3 costs include net direct cash costs, depreciation and amortization, indirect costs, and net interest charges. We obtained firm-level cost data from supply-chain analytics provider SC Insights for Q1 2026 with production forecasts through 2035. We collected ownership data from SCI Insights and supplemental publicly available sources when this information was unclear from existing asset-level details. Researchers leveraged a semiautomated data collection pipeline that programmatically queries open web sources and extracts structured data using a large language model. All machine-generated outputs were reviewed by an author and cross-referenced against company reports and live open sources. from SC Insights to illustrate several important aspects of the market. We also collected ownership data to show that market concentration reflects not just where the production occurs but also who owns the assets.

Figures 2 and 3 show projected aggregated production weighted average C3 cost and forecasted lithium processing capacity in 2030, grouping mining assets into different country and ownership categories. Several findings emerge from these figures.

First, as demonstrated in Figure 2, domestic investments of lithium in the Chinese mainland are not necessarily competitive. However, once ownership status is accounted for, the competitiveness of Chinese assets in the upstream lithium market improves. Second, though the United States averages lower costs than domestically extracted Chinese lithium, mining is more expensive than all other sources; this includes Chinese-owned assets outside of China, global averages (including China), and nations participating in FORGE.

Figure 2. 2030 Lithium Extraction Cost Competitiveness by Bloc and Ownership Status

Note: Aggregated production weighted average C3 cost across countries, national blocs, and plurilateral agreements or summits of interest. The Critical Minerals Ministerial was not a formal agreement but rather a summit at which future coordination between the United States and attending nations is not ensured. The Pax Silica agreement is excluded because assets are the same as MSP/FORGE agreement.

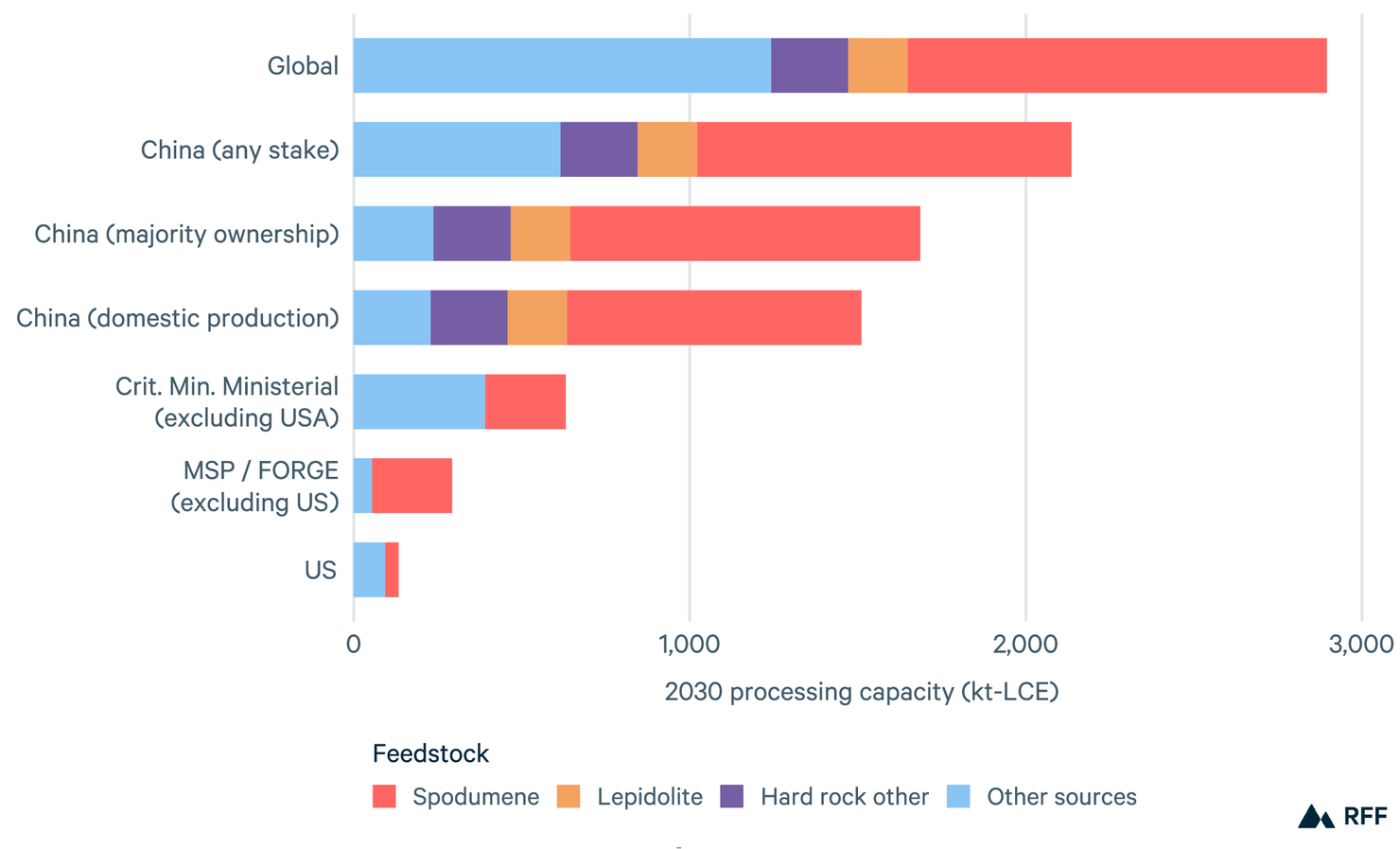

Third, supporting battery material supply chains from existing domestic and FORGE-affiliated hardrock lithium extraction assets is structurally limited by downstream processing capacity. Countries participating in FORGE have cost-competitive hardrock projects, but these require more complex processing to yield battery materials. As shown in Figure 3, these processing capacities are dominated by China, reflecting its comparative advantage in battery material supply chains. The vast majority of FORGE assets are hardrock projects, indicating that future plurilateral agreements on battery material sourcing would benefit from coordination with lithium brine–producing nations, like Argentina and Chile, which are not part of FORGE.

Global DLE projects appear to be competitive and offer a more ready end-to-end supply-chain solution given China’s advantage in hardrock processing. Finally, countries that participated in the high-profile Critical Minerals Ministerial include those with highly competitive assets, but coordination with them on diversifying processing capacities is uncertain.

Figure 3. 2030 Projected Lithium Processing Capacity by Bloc

Note: 2030 projected lithium processing capacity from SC Insights (2025), including operating and highly probable assets.

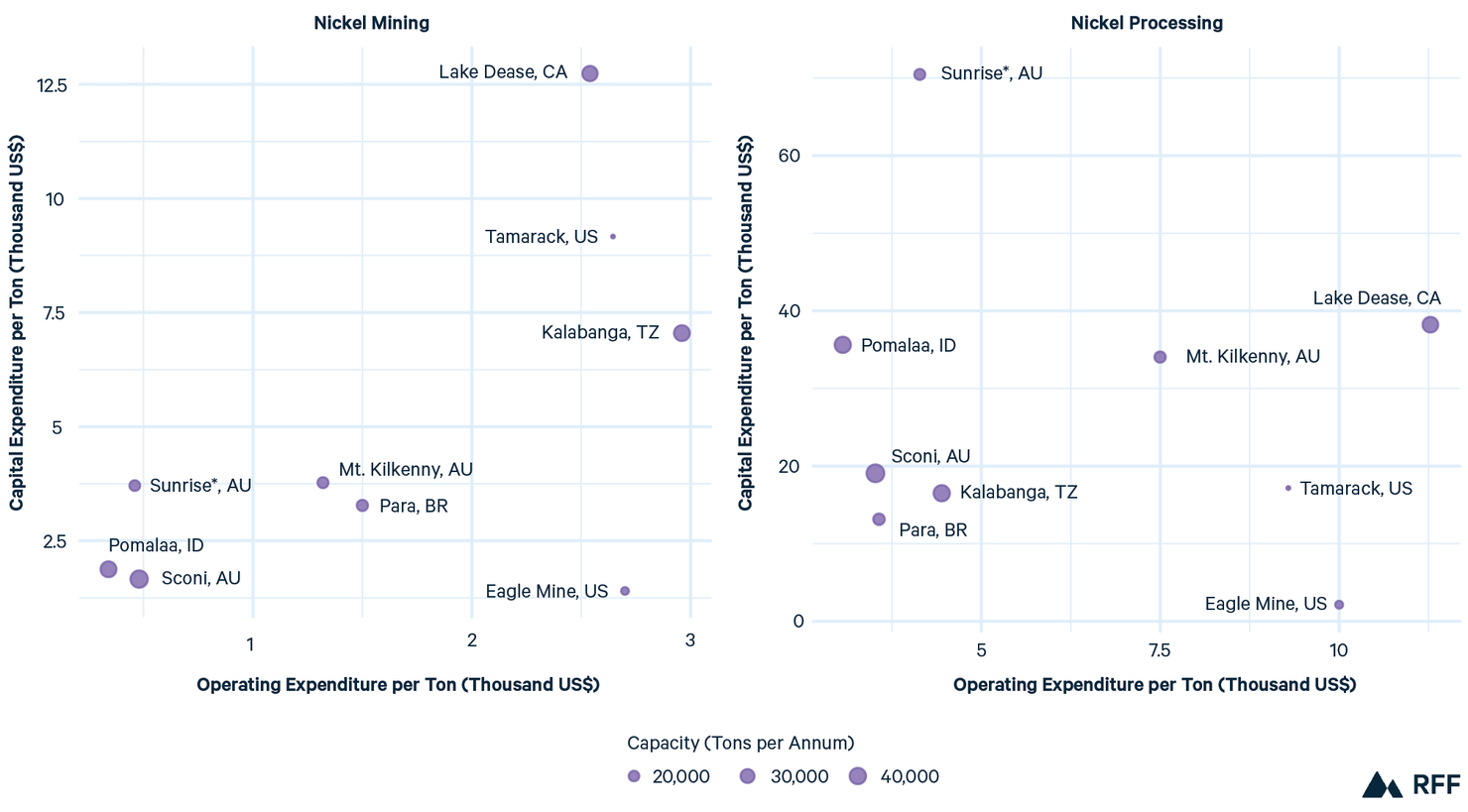

2.1.2. Nickel

Nickel is primarily extracted from laterite ores, found predominantly in countries such as Indonesia and Australia, though deposits of magmatic sulfide are more common in the United States and Canada. The ores are processed through smelting, which also yields valuable coproducts—including copper, cobalt, and platinum—to offset production costs. Producing nickel sulfate this way requires high-pressure acid leaching (HPAL), which can process low-grade ores (as low as 0.9 percent) into battery-grade nickel at about half the cost of processing nickel from magmatic sulfide deposits (Mills 2024; MiningVisuals 2025) (Peers Solutions 2025). However, this low cost comes with a large environmental trade-off. HPAL uses sulfuric acid for leaching and produces magnesium sulfate as tail-waste; reporting has found that many operating plants dump these into the oceans (deep-sea tailings) (Ribeiro et al., 2021; Geiger 2021). Heap leaching, an alternative processing method used in Mt. Kilkenny, Australia, is less environmentally invasive, requiring lower volumes of water and energy, but much slower and has lower production capacity.

Despite a small number of laterite deposits in the United States, HPAL would likely lack social license because of its high-power demand and toxic waste streams.

Figure 4. Nickel: Capital Expenditure Versus Operating Expenditure

The United States has limited nickel reserves and only one operating mine, which is nearing its end of life: the Eagle Mine in Michigan. It does not have on-site refining capabilities and relies on Canada, which significantly reduces its capital intensity.

Projects under development include the Tamarack mine in Minnesota and the Nikolai mine in Alaska, both of which include processing. As of early 2026, the Tamarack project has completed the feasibility phase and is moving forward with commissioning. It is expected to produce the majority of the future domestic supply of battery-grade nickel, and the company has an offtake agreement with Tesla that supports its financial viability. However, additional supply may emerge from the Eagle Mine. Talon Metals Corp (the owner of the Tamarack project) recently purchased the mine and its processing mill from Lundin, and its existing exploration in that area suggests an effort to extend the life of the operation (Talon Metals Corp. 2026).

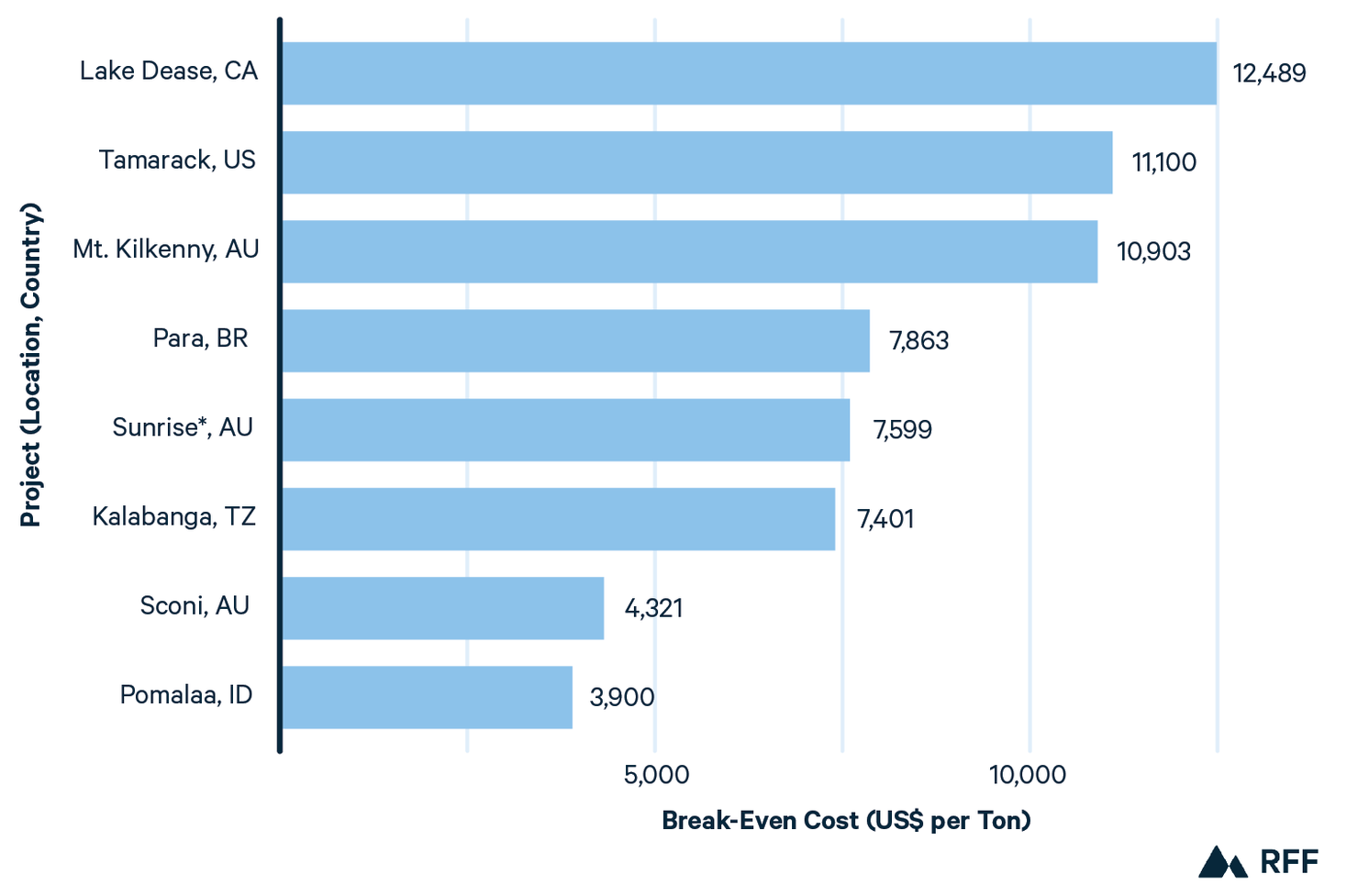

Figure 5 compares the break-even cost per ton for several projects discussed. We include only those that have these values listed in their reports. The Tamarack project is on the higher end of the distribution. The two lowest-cost projects are laterite and rely on HPAL, highlighting the cost–environment trade-off associated with that processing approach.

Figure 5. Nickel Projects: Break-Even Cost per Ton

Note: Source data come from feasibility and project studies. See Appendix for list of projects used.

A coproduct that is generally mined along with nickel—and rarely mined as a primary resource outside of the DRC—is cobalt. Such production illustrates how critical mineral markets are interrelated, as the majority of operations producing cobalt must justify investment decisions accounting for market dynamics for a separate commodity. A rare example of a US mine developed primarily for cobalt extraction was Jervois in Idaho, which was deemed financially viable at 2022 cobalt prices. However, after investing approximately $150 million in it (including $15 million from DOD for a refinery), the company was forced to idle production and lay off workers when cobalt prices dropped significantly in 2023 (Reuters 2025).

2.1.3. Graphite

Graphite can be produced either synthetically—by heating petroleum coke or coal tar pitch to extremely high temperatures—or naturally by mining. Synthetic graphite has higher purity and generally results in better EV battery performance. It accounted for 80 percent of the global EV battery market in 2022 (Rystad Energy 2023). In contrast, natural graphite has a lower cost; some battery manufacturers therefore blend the two.

On the synthetic side of the market, US producers face a disadvantage due to higher costs of raw materials and energy and lack of offsets from the sales of secondary products for low-grade applications. Bhuwalka et al. (2025) estimate that Chinese production costs are $2,500–3,500 per ton, compared to $12,000–16,000 per ton in the United States. This gap allows Chinese producers to price graphite at $6,000–8,000 and achieve comfortable margins but renders US producers uncompetitive. Recognizing the lack of competitive domestic supply, both the Trump and Biden administrations exempted graphite from the FEOC restrictions to allow US automakers to continue manufacturing EVs (Graphite Alliance 2024).

When it comes to domestic natural graphite production, Alaska has substantial deposits. Graphite One, a junior mining and processing venture, aims to begin producing in 2030, though it has faced considerable opposition from local and tribal communities due to lack of consultation (Herz 2023, Grist 2025). Nevertheless, the US government supported the project through a DOD grant of $37.5 million, a potential Export-Import (EXIM) Bank financing deal for up to $2.07 billion toward mining graphite and advanced material manufacturing, and fast-tracking approval for permits (Graphite One 2023, 2025a, 2025b), citing national security needs. The project is being expanded in capacity and expected to operate for 20 years.

2.1.4. Rare Earth Elements

REEs are a group of 17 critical minerals that, despite their name, are not geologically scarce but tend to be less concentrated in deposits worldwide. They are increasingly demanded for high-performance magnet applications, which account for 95 percent of their consumption by value (IEA 2026). They are divided into light (LREE) and heavy (HREE) categories based on fundamental atomic differences and found in different types of mineral deposits (Critical Strategic Metals n.d.). For instance, carbonatite deposits (like those at the Mountain Pass mine in California) are sources of LREEs such as neodymium and praseodymium (Van Gosen et al. 2017). HREE deposits are typically sourced from peralkaline intrusions and increasingly from xenotime-monazite accumulations (Richter et al. 2018). The mineralization of rare earths is complex, but distinguishing between LREE and HREE is important for supply-chain resiliency and targeted policies. Dysprosium and terbium, both HREEs, are used to improve the high-temperature performance of rare-earth permanent magnets; LREEs are used to provide high magnetic strength.

Comparing the costs of REE extraction projects across different countries is inherently challenging due to a complex interplay of factors. Apart from the significant variety of REEs and variations in deposit mineralogy (which impact processing requirements), the presence of naturally occurring radioactive materials introduces unique technical and financial hurdles. Project-specific product mixes and pricing structures add complexity, making it challenging to establish a break-even or all-in sustaining cost for discrete REEs. As the later discussion demonstrates, these factors help explain why cost comparisons between nations or plurilateral blocs are rarely straightforward and often require a nuanced, project-specific technical analysis.

A major driver of cost variance is processing intensity—that is, the costs attributed to chemical reagents, thermal and energy demands, waste handling, and the capital-intensive equipment required to concentrate an end product for the next step of the supply chain. Carbonatite deposits of LREEs are more straightforward to process than peralkaline intrusions, which require more intensive metallurgical cracking to liberate and separate the HREE metals. The processing intensity of removing impurities and separating out lower-value elements (which may have productive uses in their own right) is important because the economic viability often hinges on the market price of higher-value HREEs, like dysprosium and terbium.

Most REE deposits also contain naturally occurring radioactive materials, like uranium and thorium. These can change a project’s outlook because of the costs and social license considerations of additional safety measures and more stringent waste-handling protocols. In some cases, producing uranium can provide a partial cost offset for the mine. By contrast, thorium typically has low commercial value. For a real-life example of how radioactive materials can change project outcomes, the Kvanefjeld project in Greenland was viewed as financially attractive in part because its base-case economic scenario included revenues from uranium sales in addition to REEs. When the Greenland government decided to halt all mining of radioactive materials in the country, the project was terminated (Wood Mackenzie 2026).

Figure 6. Rare Earth Elements: Capital Expenditure Versus Operating Expenditure

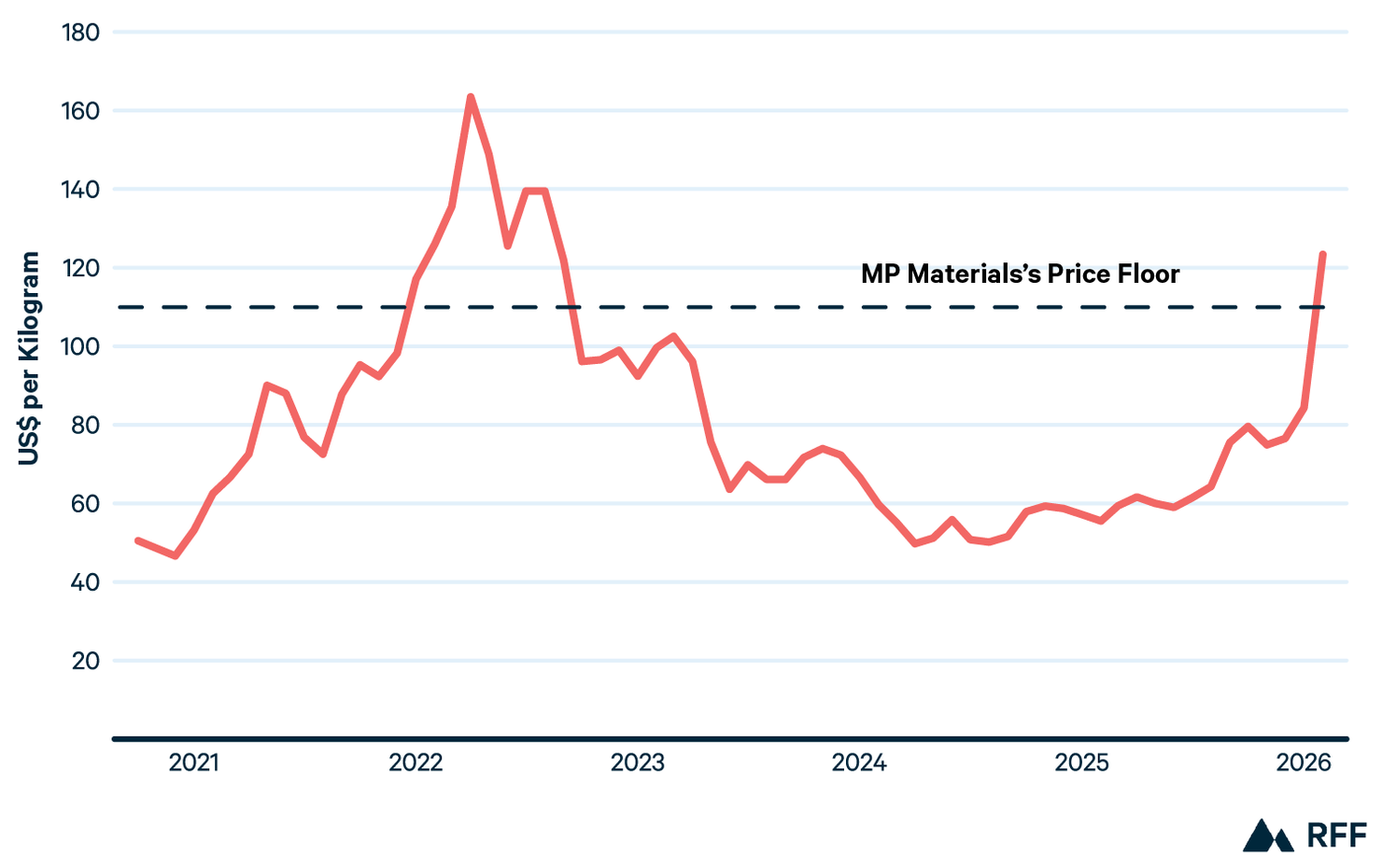

All of these complexities mean that project viability is often evaluated across many potential product mixes, which makes it extremely difficult to ascertain a single break-even/all-in cost. For example, the total rare earth oxide “basket” can include compounds like lanthanum oxide and cerium oxide, which are traded at approximately $1,800/ton, and neodymium-praseodymium (NdPr) oxide, which in recent years has traded around $60,000/ton (USGS 2026). Prices for NdPr oxide—a primary input to rare earth permanent magnets—are highly volatile (see Figure 7). As a result, projects that appear attractive under optimistic assumptions can fail to advance due to mounting financial risks and a volatile commodity price market.

In July 2025, DOD partnered with MP Materials to accelerate domestic magnet production by providing a $150 million loan, purchasing $400 million in convertible preferred stock, and signing a 10-year offtake agreement to purchase all the produced magnets, with a price floor of $110/kg (Kannan et al. 2025), which was approximately double the prevailing market price, suggesting that the operation was not economically viable without significant government support. Although the price has surged in 2026 to levels far exceeding the floor, the historical price volatility means that the deal’s ultimate cost to the government remains uncertain.

Given the complexities in extracting REEs, efforts to do so from mine wastes are ongoing. However, the costs may not be viable. We discuss this further in Section 3.2.

Figure 7. Rare Earth (Neodymium-Praseodymium [NdPr] Oxide) Prices from 2021 to 2026

2.2. Midstream Gaps and Demand Uncertainty

2.2.1. Midstream Gaps

A significant gap in the US critical mineral value chain lies in the midstream, which includes refining, processing, and component manufacturing. Refining and processing convert milled ore into battery-grade materials, and the United States remains heavily dependent on foreign capacity (Federal Consortium for Advanced Batteries (FCAB) 2021).

China controls 70 percent of global cobalt refining and 90 percent of REE separation and oxide concentration (Ijjasz-Vazquez et al. 2026; Allan and Goldman 2025). As noted, the nickel and cobalt extracted at the Eagle Mine in Michigan are exported to Canada for refining (Clarke et al. 2022). Similarly, MP Materials shipped its domestically extracted REEs to Shenghe Resources, a minority partner based in China; exports ended in 2025 after China’s 125 percent import tariffs on US goods (Mining Engineering 2025; Luk 2025).

Despite efforts to invest in domestic battery manufacturing, significant gaps remain in component manufacturing. Globally, the United States accounts for only 10 percent of anode, 2 percent of electrolyte, 6 percent of separator, and 0 percent of cathode manufacturing capacity (FCAB 2021). As a result, battery manufacturing costs are higher. Benchmark Intelligence (2023) estimates that producing EV batteries is 46 percent more expensive in the United States than in China.

Rare earth magnets present a similar challenge. US processing capacity remains limited—for example, in 2023, DOD entered into an agreement with E-VAC Magnetics to produce 1,500 tons per annum (TPA), though the country as a whole was importing 40,000 TPA, most of which came from China (producing 240,000 TPA; Rare Earth Exchanges 2026, DOD 2023). China’s vertically integrated supply chains and large-scale processing capacity has allowed it to lower operating costs and amortize fixed costs across large volumes. This has contributed to a substantial cost advantage: China can separate rare earth oxides at $2,000–4,000 per metric ton; costs in Western countries can exceed $10,000 per metric ton (Discovery Alert 2025; Tiron 2025).

Lynas, an established REE producer, provides a useful example. It operates a mine in Mt. Weld in Australia and processing facility in Malaysia and sought to open a magnet facility in Texas, receiving approximately $258 million in support from DOD. However, the Texas facility faced significant hurdles and cost overruns of up to $170 million (Lynas Rare Earths 2023). This suggests that US capital intensity is much higher than in other regions, especially Asia.

2.2.2. Demand Uncertainty

US EV adoption grew from less than 1 percent in 2016 to 10 percent in 2025 (Argonne National Laboratory n.d.). Though part of this growth reflected the rising popularity of Tesla vehicles, federal and state-led policies (e.g., tax credits, emissions standards, state-level EV mandates, and charging station subsidies) also played an important role. As described in Section 1.4, the IRA expanded EV purchase subsidies, increasing demand while incentivizing domestic battery manufacturing. After the change in administration and the reversal of the IRA tax credits, many manufacturing and production targets were revised downward (Ozsevim 2025).

Although some of the experts we interviewed criticized the stringent domestic sourcing requirements in the IRA tax credits as unattainable in the short run, many expressed concerns about their reversal. They also cautioned that the lack of policy continuity across administrations increases investment risk and undermines long-term incentives across the supply chain and viewed the administration’s simultaneous removal of demand-side incentives and increase in extraction incentives as internally inconsistent.

Without demand-side incentives, opportunities to secure offtake agreements reduce, limiting mineral producers’ ability to obtain higher and more stable prices—a necessary condition for many investment decisions. One notable example of this interaction is the deal between Lithium Americas and General Motors (GM). In 2023, GM invested $650 million in equity into Lithium Americas’ Thacker Pass and signed a binding 10-year offtake agreement for enough lithium to produce 1 million EVs per year, with the option to extend (Lithium Americas 2023). In 2024, the companies restructured into a joint venture, with a new $2.3 billion DOE loan; GM agreed to a 20-year 100 percent offtake agreement (Lithium Americas 2024).

In 2025, after the significant changes in federal EV policy and GM’s own backtracking on EV targets, DOE took an equity stake in Lithium Americas to draw down the DOE loan. As part of the revised agreement, GM withdrew from its offtake commitment, allowing Lithium Americas to “enter into additional third-party offtake agreements for certain remaining production volumes not forecasted to be purchased by GM” (Lithium Americas Corp 2025). This episode illustrates how reductions in demand incentives weaken the incentives for long-term offtake agreements.

3. Technical and Infrastructure Challenges

3.1. Workforce and Expertise

The mining industry faces a human capital constraint. A McKinsey survey of major mining companies across Australian, North American, and Latin American markets identifies issues across the talent life cycle, including a decline in talent acquisition from major engineering programs (Abenov et al. 2023). Companies are reporting a declining interest from younger individuals. Rio Tinto (2023), an international mining company, wrote in an annual report that “As societal expectations are changing… without change or action, our ability to attract and retain partners and talented people will be negatively impacted.” In 2022, the president of Freeport-McMoRan stated that the firm could have produced more copper if it had sufficient staffing (Scheyder and Kumar 2023).

Supporting the onshoring of the mineral supply chain will require workforce development in two major areas: science and engineering and professionals in trade. With respect to STEM training, the Society for Mining, Metallurgy, and Exploration, an industry association, has been advocating for more support to the nation’s higher education institutions for at least a decade, remarking in a 2022 report that the number of accredited mining engineering programs has dropped from 25 in 1982 to 14 in 2020 (SME 2022). In 2023, only 312 mining engineers graduated from US universities, prompting some firms to support workforce development programs directly (SME 2025; Thorburn 2025; Albemarle 2024). Other types of scientific training are needed as well, such as geologists and process and chemical engineers. Recent work has identified the role of facilitating partnerships between industry and academia, despite little cross-industry consensus on where specific efforts should be directed (Mehta 2024).

In the short run, attracting highly trained STEM professionals from other countries could solve the skill gap as the domestically trained workforce is built. However, the ongoing federal crackdown on partnerships with Chinese battery manufacturers and restrictive immigration policies have made these approaches challenging (Elliot and Stockman 2025; Gardner and Hermani 2025).

Much of this report has contrasted domestic mining and minerals processing capacity with China, which has a comparative advantage in producing raw materials. The workforce aspect is no different. The largest minerals engineering program in China enrolls 1,000 undergraduate and 500 graduate students (Hale 2023), likely exceeding enrollment in all US mining programs combined, even as efforts to support the sector ramp up at the federal and state levels.

Efforts to train the next generation of mining and minerals processing engineers also face uncertainty from technical change. The work of future extractive industries in the United States may look very different. For example, DLE extracts lithium from brines using a process more similar to the oil and gas industry than to conventional open-pit mining or evaporation-based methods. Policymakers should be attentive to the specific technologies they aim to scale and build human capital programs around the labor required to support the development.

As noted, the second major area of needed workforce includes skilled trade workers, such as plumbers, technicians, operators, and construction workers. States have taken the lead in developing targeted programs. For example, in Arkansas, the LiTHIUMLEARNS program provides a pathway for local students to acquire technical degrees for industry employment; LiTHIUMWORKS provides a platform for producers to hire local professionals in trade. For more, see https://www.lilearnsliworks.com/. A similar program in Imperial County, California is the Lithium Industry Force Training Program, a partnership between lithium producers (Controlled Thermal Resources, Berkshire Hathaway Energy Renewables, and Energy Source Minerals) and the Imperial Valley College, which offers one-year certificate programs. For more, see https://www.imperial.edu/academics/lift.html. Given the shorter timeline it takes to build up these skills, this is likely a lower hurdle to overcome compared to developing specialized STEM expertise.

3.2. Alternative Sourcing

Existing waste streams from both active and inactive/abandoned mine sites present a potential US source of critical minerals. Recent literature has estimated that the country could meet nearly all of its demand—or at minimum, eliminate all imports—by simply increasing recovery of existing by-products (Holley et al. 2025). Many critical minerals are by-products of base metals refining, and federal investments have focused on maximizing recovery from existing operations, such as the US government support for Alcoa’s gallium recovery capabilities at an alumina refinery in Australia or at ATALCO in Louisiana (Alcoa 2025; Monks and Gould 2026). Such colocation also can reduce the environmental damage associated with greenfield development. However, exploiting these resources requires significant and site-specific geometallurgical research and is often uneconomical (Holley et al. 2025).

The DOE’s Carbon Ore, Rare Earth and Critical Minerals (CORE-CM) Initiative provides a useful example of the challenge in quantifying the costs associated with commercializing by-product recovery. The first round of projects funded interdisciplinary groups of researchers across 13 US basins to study the challenges to recovering critical minerals from mine wastes (NETL 2021). However, even as these efforts advanced the understanding of the science around by-product extraction, they could not produce robust estimates of the economic costs to extract critical minerals from coal wastes.

Conversations with industry experts also highlighted the economic challenges of mining from waste streams from the perspective of commercial entities, including (1) low mineral concentration in large quantities of mine waste, requiring significant materials handling costs with limited revenue potential; (2) the need for additional infrastructure to refine extracted minerals to meet resale standards, as a company may need to add a new line of processing equipment for every one or two additional elements it wants to extract; (3) the substantial infrastructure required for limited resources, whereas similar investments in greenfield mines could result in larger resource potentials; and (4) that some operating mines are far along in their planned life and would need to be replaced to maintain production. Due to the lack of commercialized remining sites, economic viability has not yet been proven at scale. Industry participants also noted that the expertise in processing for certain by-product minerals, such as bismuth, is extremely limited domestically, which constrains the ability to pursue such projects even when potential exists; the literature also supports this challenge (Holley et al. 2025).

Remediation and remining faces significant permitting and legal uncertainties; the Environmental Protection Agency (EPA) Good Samaritan program is designed to work through these institutional frictions but is still in a pilot phase (EPA 2024).

Future programs could emphasize demonstration facilities and short-term production targets, with dedicated funding to scale successful projects that could include government offtake agreements or preferred equity to signal long-term commitment. In the interim, DOE continues to support select CORE-CM basins and fund innovative approaches to raw materials sourcing that leverage waste streams and other alternatives to primary extraction (DOE 2025a, 2025b).

The CORE-CM program and recent DOE announcements suggest that government outlays are typically directed toward research on fundamental materials science and early-stage technologies rather than rapid deployment of new capacity. Though this focus on research and development aligns with the DOE’s traditional role in supporting early-stage innovation, Biden-era efforts to expand the Loan Programs Office indicated a shift toward expanding resources for commercializing new technologies. State capacity is limited, so this shift in focus could come at the expense of the existing research and development capabilities. However, scaling innovative technologies that allow the industry to extract, process, and produce minerals and materials at low cost—and without sustained subsidies—is key to building a resilient supply chain.

Because conventional mining and minerals processing entail significant environmental impacts, one may assume that alternative sourcing reduces those impacts. All large-scale industrial installations induce environmental change, and innovative new methods of extraction may introduce their own impacts, many of which are poorly understood. Different DLE methods, for example, have different freshwater use profiles (Vera et al. 2023). Policymakers should therefore consider simultaneously funding research on environmental impacts, as communities across the country will have many questions about new industrial projects.

4. Timeline Challenges and Need for Community Buy-In

4.1. Permitting and Project Development

One challenge in ramping up domestic extraction is the long development timeline for new mines. For example, S&P Global (2024) reported that US mine development times were the second longest in the world, averaging 29 years. Their dataset included only three operating mines and all nonoperating US mines, which could bias their analysis. Although permitting is frequently cited as the primary source of this delay, estimates of its contribution vary widely.

In 2015, the National Mining Association commissioned SNL Metals & Mining to examine the costs of permitting delays. The report’s executive summary states that securing the permits necessary to operationalize a mine takes 7–10 years on average, but this is not well substantiated in the report. The report offers no citations or discussion for this claim, and this number is not developed within the report. It also includes a disclaimer noting that it is based on information and data provided by third parties and that SNL Metals & Mining did not independently verify these. More recent analysis presents a different picture. The Biden-Harris administration’s Interagency Working Group on Mining Laws, Regulations, and Permitting published a report assessing how to improve mining on public lands (IWG 2023). In contrast to S&P Global’s claim, the report stated that the total time between exploration and commercial production averages 16 years, with permitting accounting for a small share of this. IWG reached this conclusion based on two data sources: GAO (2016) and EPA’s National Environmental Policy Act (NEPA) records. GAO finds that permitting times take about 2 years, and EPA’s records shows that the average Environmental Impact Statement—a key part of the permitting process—takes less than 5 years. However, the IWG did not analyze these times separately for large or small mines or include state-level time frames; these could vary significantly by state due to differences in the processes, such as the stringency of environmental permit provisions. The IWG attributed long development timelines primarily to litigation and incomplete operational plans.

Thus, how much permitting delays mine development remains an open question that warrants further research. What is clear, however, is that the timelines for operationalizing a mine are long. This is not unique to the United States (European Court of Auditors 2026; Johnson et al. 2023; Green and Jackson 2017) but it is especially challenging in a market characterized by high risk and uncertainty. Price volatility, in particular, complicates investment decisions: from an economics perspective, opening a mine makes sense when prices support the financial viability of the project. Yet, by the time the mine is operational, prices may have drastically changed, leading to mine closures (as illustrated by the Jervois cobalt mine; see Section 2.1.2).

Rapid technological change presents additional risk, as demand for certain minerals may decline. For instance, many EV manufacturers (and battery energy storage plants) are shifting to LFP batteries, which require no cobalt. Although such changes can be difficult to predict, some are foreseeable and should be considered when designing policies to support mining investments.

Accelerating mine development also requires looking beyond permitting. For example, the USGS, in partnership with State Geological Surveys, developed Earth MRI, a new system for mapping critical mineral deposits using geochemical sampling and other advanced measurement techniques (USGS 2025), which could reduce exploration times. However, its funding is limited. The IIJA provided $320 million over 5 years (USGS 2022), which is modest compared to exploration expenditures by private companies on individual sites. These funds are set to expire in September 2026.

Relatedly, though the recently passed Critical Minerals Dominance Act See https://www.congress.gov/bill/119th-congress/house-bill/4090. directs the DOI to accelerate the geological mapping, no funds have been allocated to support this. Furthermore, the USGS has lost 1,700 workers between 2025 and April 2026 (OPM 2026), raising questions about its capacity to ramp up its mapping capabilities.

4.2. Lack of Effective and Equitable Community Engagement

As the IWG noted, litigation against mines is common. This can occur when participatory engagement with local communities is absent or lacking. Meaningful engagement requires the mining company to maintain an active, positive, and sustained relationship with communities throughout its presence in the area—from exploration to mine closure (Fraser et al. 2019). Such engagement allows communities to express their concerns, suggest changes that reflect their local priorities and values, participate in benefit sharing, and benefit from pollution mitigation. In turn, this can help secure a social license to operate and reduce litigation risk (Prno 2013).

Achieving social license to operate can also reduce the risk that local communities block development altogether. This outcome has occurred both globally and in the United States. One example is the Pebble Mine in Alaska’s Bristol Bay region, an area that had a large deposit of gold, copper, and molybdenum but was also an active salmon fishery. The mine was expected to destroy 81 miles of salmon streams, prompting large and active campaigns against it by local Indigenous tribes, the commercial fishing industry, and tourism and recreation stakeholders. This coordinated local opposition led to multiple lawsuits, resulting in EPA vetoing and the Army Corps of Engineers denying the permit (Brooks 2025; Holley and Mitcham 2016). Other domestic projects that have faced similar challenges due to social license failures include the PolyMet and Twin Metals copper-nickel mines in Northern Minnesota (Frank 2020; Green 2022) and Resolution Copper mine in Arizona (Sherman 2025; Grijalva 2025; Gila Herald 2026).

Effective and equitable participatory engagement is not widespread. Yet, if mining is to proceed in a manner that respects, protects, and benefits surrounding communities, it should not be overlooked. The Biden administration implemented policies related to clean energy investments that aimed at addressing this gap. For example, projects receiving federal funding through the IIJA and IRA were required to develop a community benefits plan (see NARUC, n.d.). It required engagement with the community and labor groups and encouraged community oversight of the projects, which could lead to reduced environmental impacts for mining.

Such agreements—sometimes labeled as benefit sharing agreements, community benefit agreements (CBAs), or impact benefit agreements (IBAs, which typically focus on impact mitigation)—are common mechanisms for engaging with local communities and can take many forms. However, they do not always ensure effective, equitable, or participatory engagement. Though many guidelines exist to create them (e.g., Gibson and O’Faircheallaigh 2015, Cascadden et al. 2021; Eisenson and Webb 2023), achieving meaningful participatory engagement requires more than a well-structured agreement. It requires a sustained relationship with the communities throughout the lifetime of the mine and mechanisms that allow them to give input, be heard, participate in decision making, and truly benefit from the development (Spiller et al. 2025b). This takes time and deliberate action by the company, community, and governments at all levels.

Fast-tracking development and sidestepping community engagement is likely to result in outcomes where communities receive no benefits from and have little influence over local development and face increasing marginalization. The likely outcome is increased conflict and a lack of social license to operate, leading to lawsuits and delays (Ruple and Race 2019; Ciftci and Lemaire 2023; Eke et al. 2024). In this sense, efforts to expedite development may not shorten overall timelines. This underscores the need for caution when developing policies that prioritize speed of development at the expense of community engagement.

5. Policy Landscape and Insights

5.1. New and Emerging Policy Tools

The Trump administration has characterized reliance on Chinese suppliers of critical minerals as a dependence on “hostile foreign actors” constituting a national emergency. See evocation of the National Emergencies Act (50 U.S.C. 1601 et seq.) in the administration’s January 2025 executive order, Declaring a National Energy Emergency (90 FR 8433). In response, it has pursued a range of measures, including tariffs, deals with individual firms (both domestic and abroad), international cooperation, stockpiling and industry investment funds, and permitting reform to diversify supply and expand domestic extraction; we discuss these new and emerging tools next, with their potential ability to affect the domestic minerals industry.

5.1.1. Tariffs

Tariffs presumably are an approach to equalize costs across countries by raising the price of imported minerals, thereby allowing higher-cost domestic producers to compete. However, their effectiveness relies upon several strong assumptions. First, domestic production must be able to expand rapidly; otherwise, tariffs will simply increase costs while the industry continues to rely on imports. Second, demand for minerals must be inelastic. If demand is inelastic, the tariff is passed through entirely to the consumer, raising the imported mineral price by the magnitude of the tariff. However, if demand is elastic, the price of the mineral will increase by less than the full amount of the tariff, limiting the benefit to the domestic producer. Either way, tariffs create upward pressures on consumer product prices, creating a tradeoff that must be taken into account by policymakers, particularly during times of affordability crises. While tariffs have the potential to improve the cost competitiveness of domestic mining if these conditions are met, other policies are likely to result in fewer unintended consequences under more realistic scenarios.

Volatility in the copper markets has underscored how broad tariffs can disrupt bilateral trade flows and raise costs for downstream products (Balleny 2025). Even targeted tariffs (like those for graphite active anode material) have generated controversy because of implementation challenges and the differing business models across domestic firms in the supply chain (Cefai and Raboca 2024). Finally, tariffs on a specific mineral, particularly those with large markets (such as copper or aluminum), are unlikely to be viewed as politically durable even within a short time frame, let alone across administrations, thereby reducing their ability to incentivize capacity investment in the long run.

Another challenge with import tariffs is that some minerals, such as aluminum or sulfur, are intermediary inputs to construction and processing. Tariffs would thus increase the cost of building and manufacturing domestically, slowing the growth of the domestic supply chain.

5.1.2. Public Investments in Private Enterprise

Financial interventions into individual firms have included equity stakes and price floors, such as the equity deal with Lithium Americas and price floor provided to MP Materials (see Section 2). These policies have been reserved for firms in crisis, as with the automotive industry in 2008 or Conrail in the 1970s (CBO 2021; Webel et al. 2020). Their application in emerging industries therefore represents a notable departure. A report by Securing America’s Future Energy notes that some critical mineral markets, like gallium and germanium, have such small demands that firm-level price measures may meaningfully reduce market concentration—especially when allied countries adopt similar measures (SAFE 2025). Bloomberg reported that in 2025, the US government spent over $1 billion in equity stakes in mining companies (Natter 2025).

Baskaran (2024) also notes that government equity can signal long-term commitment to a project and crowd in private investment. A recent public–private partnership is the $7.4 billion Korea Zinc smelter in Tennessee, financed by the US government and JPMorgan’s new Security and Resiliency Initiative (Lorinc et al. 2025; JPMorganChase 2025). However, firm-level support does not guarantee a project’s success, especially in a sector with such challenging fundamentals. As described in Whitlock et al. (2026) and elsewhere in this report, project outcomes depend on factors such as community approval, workforce readiness, and cost competitiveness.

Palladino (2024) offers a different perspective on government equity stakes that goes beyond financial returns. Rather than serving solely as a profit-sharing mechanism, these could allow agencies to participate in corporate governance and advance public-interest objectives. For mines and heavy industrial projects like minerals processing, which entail significant impacts to communities, such tools could improve a project’s social license and support democratic deliberation on environmental impacts and CBAs.

The expansion of state financing authorities for mining and processing projects is notable and outlined in some detail by the administration in a March 2025 executive order See https://www.whitehouse.gov/presidential-actions/2025/03/immediate-measures-to-increase-american-mineral-production/. that directed new coordination between the DOD Office of Strategic Capital and the US Development Finance Corporation. Another pertinent subsection directed the bank to use the Supply Chain Resiliency Initiative to secure raw mineral resources for domestic processing capacity, though this strategy has yet to materialize at scale. The initiative itself is an example of expanding state capacities to finance extraction projects, as historically the bank focused on promoting US exports.

However, public investments in private enterprises can reduce US industry competitiveness in the long run if the chosen projects are not cost-effective to begin with; thus, investing in innovative firms could provide greater benefits, in terms of both reduced fiscal costs (as these firms would require less subsidization long term) and increased global competitiveness.

Furthermore, public investments in upstream enterprises would be best supported by policies that support downstream demand. In the Lithium Americas and GM venture, a downturn in EV demand exposed the US taxpayer to downside risk after the government’s equity stake in Lithium Americas. Supporting downstream demand creates opportunities for downstream manufacturers to enter into multiyear fixed price offtake agreements for minerals, benefiting both the mineral producers and product manufacturers by reducing their exposure to price volatility.

5.1.3. Multilateral Agreements

Unlike firm-level investments, the Trump administration’s multilateral agreements may be more supportive of the industry as a whole. One example is a meeting in January 2026 by G7 countries to discuss a harmonized price floor mechanism for REEs to protect domestic and allied minerals producers and processors from Chinese price-setting behavior (Martinez and Singh 2026). The next month, the State Department convened the Critical Minerals Ministerial, bringing together 54 countries to discuss a minerals trading bloc supported by price floors (see Section 1.3).

Although price floors may reduce the incentive to innovate and lower costs, for larger markets, multilateral action on minimum price levels could help share the costs of geographically diversifying minerals extraction and processing capacity. Recent federal actions suggest recognition of this issue; the administration held off on imposing Section 232 tariffs See https://www.whitehouse.gov/presidential-actions/2026/01/adjusting-imports-of-processed-critical-minerals-and-their-derivative-products-into-the-united-states/. on processed critical minerals in favor of further negotiations. However, although these multilateral agreements supported by price floors could help geographically diversify the supply of minerals, no reason exists to expect that US capacity will be built up, given the challenges and increased costs of building domestically compared to other countries party to the agreement (see Figure 3 and FORGE cost competitiveness comparison in Section 2.1.1).

The bipartisan Developing Overseas Mineral Investments and New Allied Networks for Critical Energies (DOMINANCE) Act is another example of a multilateral approach. It seeks to address China’s hold on critical mineral supply chains through international agreements, specifically by strengthening coordination between the Minerals Security Partnership Finance Network Now FORGE. See Section 1.3. and US state financing agencies. It would also create an Office of Energy Security Compacts to manage relationships with producing countries and elevate resource diplomacy in its bureaucracy.

In sum, multilateral agreements and friendshoring provide an opportunity to leverage comparative advantages along the supply chain with allied nations but reduce the likelihood of investments domestically given the high costs of domestic production. Thus, this presents a significant trade-off for the government in terms of achieving supply-chain resilience and industrial policy goals.

One major challenge of friendshoring and multilateral agreements is the requirement for policy durability to ensure entry of investment. Given the long time horizons and high costs of entering into the supply chain, investors require market and policy certainty; in the framework of a multilateral agreement, such as the price floor supported by import tariffs, the investor would require some measure of confidence that the agreement would hold long enough to allow for profitability. Yet, in a period of ongoing geopolitical tensions, the credibility of these types of agreements may not be strong enough to spur investment.

5.1.4. Stockpiling: Minimal Improvement in Demand Uncertainty

Stockpiling has emerged in recent policy discussions as a key tool to help stabilize markets in light of mineral price volatility. For example, OBBBA allocated $2 billion for this (Esmen 2025). The renewed focus is partially due to the limitations of existing programs: recent analysis has suggested the National Defense Stockpile (a strategic reserve of minerals maintained by DOD for key defense production and industrial capacity uses) faces a $15 billion shortfall in the event of a major conflict (Keys 2023). As differentiated from the National Defense Stockpile, however, recent stockpiling policies have not proposed a model where the government procures critical minerals narrowly for its own defense purposes but rather orchestrates supply contracts between US-based manufacturers and US or allied capacity. This is an important feature of a new stockpile program, as a larger Defense Stockpile would not provide the necessary quantity of minerals to support the broader minerals market (DOD’s demand for critical minerals is far lower than consumer market demand; see GAO 2024).

The federal government in January 2026 also announced Project Vault, a strategic reserve backed by $12 billion, largely through EXIM Bank ($10 billion) and some private capital ($2 billion) (EXIM 2026). Although details on how a Project Vault–style stockpile would function remain unclear, proposals outlined by Cook et al. (2025) and Datta et al. (2025)—and those formalized in the SECURE Minerals Act of 2026—envision a public corporation with a range of financial tools, among them physically settled futures contracts, nonresource lending, and contracts for differences. What the fiscal cost would ultimately be to the US taxpayer would depend on not just these structural details but also how the mineral markets develop over time.

5.1.5. Permitting Reform

Several interviewees cited long permitting timelines as a barrier but did not identify specific solutions. Passing reforms in Congress has proven challenging; the 2024 Manchin-Barrasso bill, which sought to improve permitting timelines, was ultimately not passed by Congress. More recent bipartisan legislative efforts include the Standardizing Permitting and Expediting Economic Development (SPEED) Act, which passed the House in 2025 but, as of early 2026, is expected to face challenges in the Senate (Howland 2025). Some aspects of it, such as cross-agency collaboration and concurrent reviews, could shorten timelines without undermining community engagement. However, others—particularly the proposed NEPA reforms that limit community input—raise concerns about reduced social license to operate and potential litigation-related delays. Similar concerns were expressed regarding the Critical Mineral Dominance Act, which removes regulatory processes that may have required community input or environmental review for federal lands (see, for example, NPCA 2026). More broadly, without a stronger understanding of whether permitting timelines are longer than necessary to minimize environmental and social impacts, reforms may not result in improved outcomes.

Although uncertainty remains regarding the durability of the administration’s changes to permitting processes for new mines and other major industrial projects, recent actions have sought to tighten timelines for environmental reviews. As noted in Section 1.3, the number of firms taking advantage of FAST-41 significantly increased in 2025, with 51 mining projects now participating in the program as either a covered project or a transparency project. It is not entirely clear why companies had not done so under previous administrations, although the effort to speed project approvals through statutory deadlines began during the former administration (Johnson et al. 2023). However, research has found an “inverse relationship” between the time spent on an NEPA Environmental Impact Statement and likelihood of litigation (Ruple and Race 2019), so fast-tracking may not actually increase the speed of development.

To ensure adequate permitting timelines, appropriate agency staffing is essential. Given the large reduction in DOI staffing, the ability to improve these timelines has likely diminished even further.

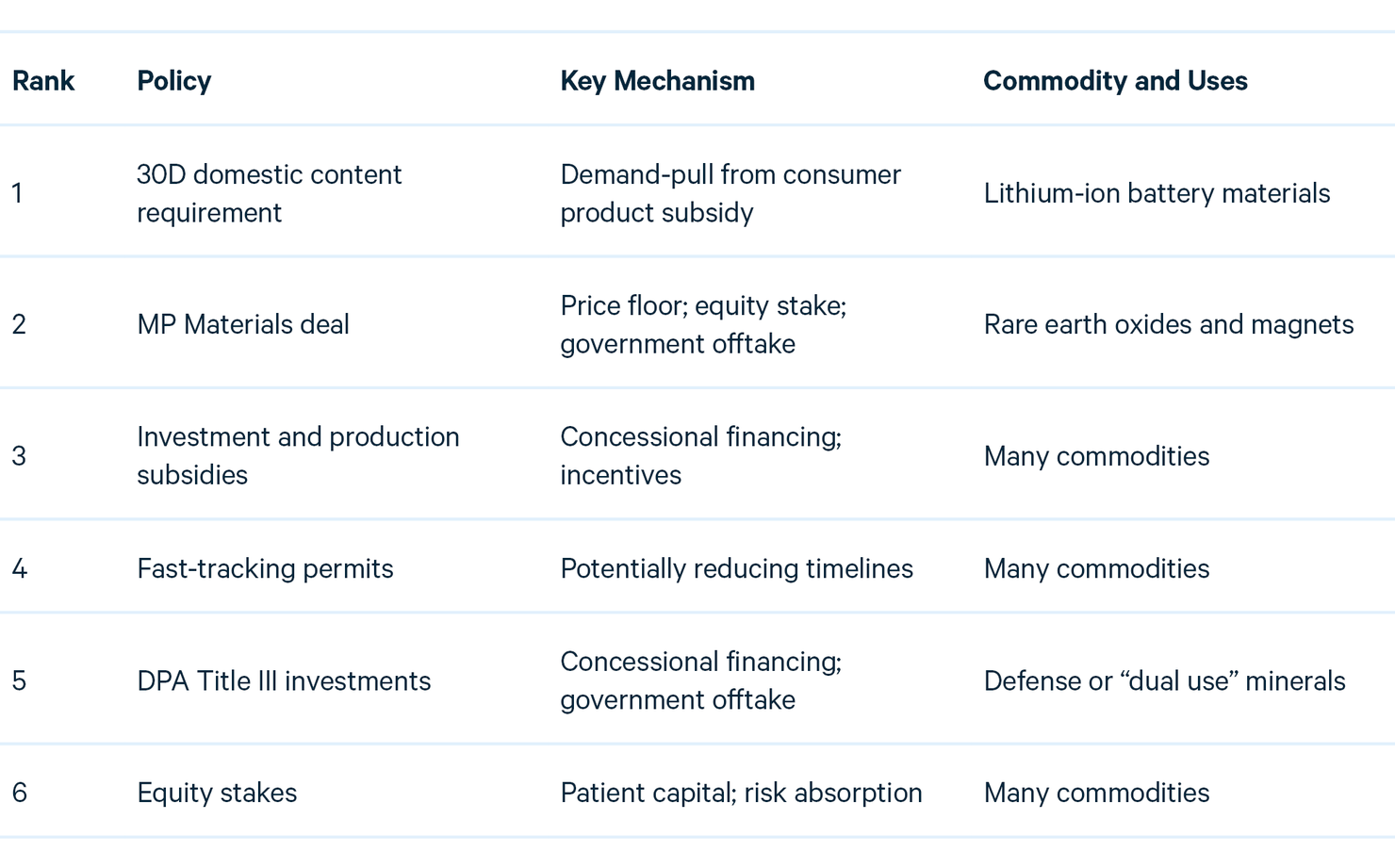

5.1.6. Summarizing Expert Responses to Policy Interventions

We compiled responses from expert interviews on government efforts to onshore critical minerals mining and processing projects. Table 1 summarizes key takeaways on recent policy instruments used to promote domestic activity, highlighting some major qualifications. The interviews focused mostly on policies before the second Trump administration (the interviews were conducted in fall 2025) and reflected uncertainty arising from the transition of critical mineral policies motivated by both decarbonization and security considerations to a more singular national security focus.

One idea that emerged in some interviews to reestablish a Bureau of Mines to help centralize government expertise and improve permitting outcomes. The Bureau of Mines, created in 1910 and abolished in 1996, was the primary government agency in charge of mineral-related oversight and analysis covering activities such as scientific research; collection, analysis, and dissemination of information; analysis of mining regulations and laws; and mining safety issues. Recent legislation has also sought to strengthen mining and natural resource expertise within the State Department and other agencies, as expanding domestic processing capacity requires sourcing raw materials from across the world (Northey 2026). However, other interviewees cautioned against this for two reasons. First, coordination would remain difficult due to the disbursed nature of critical mineral functionality and policymaking across the government. Second, key aspects of the prior bureau are already conducted by other agencies and nongovernmental organizations. Thus, the risk of duplicating efforts may overshadow any benefits achieved by coordination improvements. Though the role of a new Bureau of Mines could be significantly different from the prior version, what that could look like was not discussed.

Table 1. Influential Recent Policies on Onshoring Critical Minerals Production

Note: Ranked from an analysis of expert responses to a question on important recent policy interventions on domestic critical minerals production and processing. Ranking does not reflect an empirical evaluation, but rather individual testimonials. The table shows views of past federal efforts and does not consider recent policy changes that have yet to fully materialize, like vastly expanded state financing capabilities and international coordination on price protection.

5.2. Prioritizing Investment

Based on our research and conversations with experts, federal investments in projects would yield greatest returns to taxpayers if they have local community acceptance, are approaching workforce readiness, and are innovating along environmental and economic dimensions.