Accounting for the Carbon Price Paid in a Country of Origin Under Carbon Border Measures

This issue brief examines how carbon prices paid in a country of origin, including subnational systems, can be recognized under the EU Carbon Border Adjustment Mechanism, focusing on the trade-offs between accuracy, incentives, and administrative feasibility.

1. Introduction

With the growing number of carbon pricing policies and border measures around the world, a central challenge is determining how to account for carbon prices that are already paid in the country of origin. Border measures are typically designed to prevent carbon leakage by equalizing carbon costs across jurisdictions, but doing so requires translating diverse carbon pricing designs into comparable measures of carbon cost. Without such recognition, producers may effectively be charged twice for the same ton of carbon emitted.

As the first operational carbon border adjustment mechanism (CBAM), the EU CBAM provides a concrete framework for addressing this issue. The regulation does so by specifying that “an authorized declarant may claim … a reduction in the number of CBAM certificates to be surrendered … only if the carbon price has been effectively paid in the country of origin,” and that “any rebate or other form of compensation” must be taken into account (Regulation (EU) 2023/956 establishing a Carbon Border Adjustment Mechanism, Article 9). This requirement highlights a central challenge: determining what constitutes a carbon price that has been “effectively paid,” particularly across jurisdictions with different policy designs.

This “double counting” concern is particularly salient in a world where carbon pricing also occurs at the subnational level. In countries such as the United States, Canada, and China, carbon pricing systems often operate at the state or provincial level. As interest in carbon pricing continues to grow, partly due to the crediting mechanism of the EU CBAM (Clausing et al. 2024), the question of whether and how to recognize these subnational policies becomes increasingly important for the incentives it creates. In a country like the United States, where a national carbon price is currently politically unlikely, maintaining incentives for states to enact carbon pricing may be attractive to support emissions reductions.

Determining how to account for carbon prices already paid is not a purely technical exercise. Different approaches lead to different economic and geopolitical outcomes via spillover incentives, environmental effectiveness, administrative complexity, and international equity. More flexible approaches to recognizing carbon pricing may better encourage policy spillovers; however, this may weaken the ability of the implementing jurisdiction to protect their industry and equalize carbon costs.

This issue brief investigates how carbon prices paid in a country of origin could be accounted for under border measures, with a particular focus on subnational carbon pricing systems. We begin by discussing the relevance of subnational policies in international trade and the extent to which they already shape market access and regulatory conditions. We then outline the key challenges associated with defining “effective payment,” particularly in the context of subnational carbon pricing systems. Building on a framework proposed by Wildgrube et al. (2024), we evaluate different approaches to crediting carbon prices—including actual payment, average price, and hybrid methods—and assess how these approaches shape incentives for producers, subnational jurisdictions, and importing authorities. Throughout, we highlight the trade-offs between administrative feasibility, accuracy in measuring effective carbon costs, and the broader implications for policy design. We illustrate these issues using trade between the European Union and California as a motivating case study.

2. The Relevance of Subnational Policies in International Trade Policy

Carbon border measures are typically framed at the national level, but carbon pricing policies often operate at the subnational level. This raises the question of whether and how border measures should account for variation within countries.

While subnational governments do not set international trade policy, they do influence the conditions under which goods are produced and sold and have existing precedent for regulating product markets. Within the United States, for example, state-level regulations can often impose requirements that go beyond federal standards. As a result, imports must comply with both federal regulations and any applicable state-specific product regulations. The California Lighting Efficiency and Toxics Reduction Act, for example, prohibits the manufacturing and sale of general-purpose lights that contain certain levels of heavy metals and phthalates, also prohibited by the EU Restriction of Hazardous Substances (RoHS) Directive, even though that is not required federally (California Legislature 2007).

Subnational jurisdictions can also influence trade-relevant policies more directly. For example, California already requires a carbon border adjustment for imports of electricity from jurisdictions without carbon pricing (Pauer 2018). In another example, Canadian provinces were directly involved in negotiations of the Canada-EU Comprehensive Economic and Trade Agreement (Paquin 2025). While these examples do not imply that subnational jurisdictions control trade policy, they illustrate that subnational governments already exercise meaningful authority over product standards and some trade-relevant policies. As a result, recognizing subnational carbon costs under CBAM would not be without precedent and could be seen as consistent with existing policy practice.

3. How the Carbon Price Paid Is Determined: Considering Incentives for Exporters and Importers

Given the precedent for subnational authority over product standards and trade-relevant policy, it is useful to consider how subnational carbon pricing mechanisms could be accounted for on a practical level. Wildgrube et al. (2024) identify two ways the EU CBAM could account for a carbon price effectively paid in a third-party region, which could be used to account for subnational policies:

- One approach is the average-price method, which calculates effective payment using the average carbon price in a jurisdiction for a specified period, net of average free allocations or rebates.

- The other is the actual-payment approach, which uses the carbon costs demonstrably paid by the producer, based on documentation such as invoices, incorporating any free allowances or other compensation mechanisms.

These approaches place the methodological burden on different actors, with the average-price approach placing the burden on the CBAM-implementing country and the actual payment approach placing the burden on declarants (and therefore producers).

How “effective payment” is defined under a CBAM shapes the incentives faced by producers, subnational governments, and importers. The chosen methodology affects whether a CBAM reinforces decarbonization incentives, encourages reshuffling, or alters political dynamics within exporting countries. More broadly, there is an inherent tension between minimizing undue interference in domestic policy and ensuring lower-carbon producers are appropriately recognized.

It is important to first consider why importing jurisdictions may hesitate to recognize subnational carbon pricing in the first place. First, there can be significant administrative burdens associated with monitoring developments in carbon pricing systems, particularly when using the average price approach. Countries such as the United States, Canada, and China contain multiple state- or province-level policies that evolve over time. Recognizing subnational pricing requires tracking benchmarks, free allocations, offsets, international credits, cap adjustment factors, and other compensation mechanisms across numerous jurisdictions. For an importing authority, this creates substantial monitoring and verification burdens.

The issue of international credits might be particularly challenging as subnational jurisdictions may be less able to independently participate in the international carbon market. While subnational jurisdictions are able to participate as buyers, they are not able to authorize corresponding adjustments or have Internationally Transferred Mitigation Outcomes. Furthermore, international credits that one jurisdiction deems as credible and appropriate for inclusion in a carbon pricing system might not be considered as such by the CBAM-imposing authority. Yet, such political judgments can cause additional diplomatic sensitivities as carbon pricing design and international credits use are both issues to be nationally determined given the bottom-up logic of climate policy under the Paris Agreement.

Second, recognizing subnational carbon pricing may create reshuffling risks. If a CBAM credits subnational carbon pricing, firms may reshuffle exports from the priced jurisdiction while shifting domestic consumption toward unpriced facilities. In this scenario, emissions within the exporting country may remain unchanged, but the composition of exports may shift, limiting the environmental effectiveness of the mechanism.

Finally, there may be legitimate political sensitivities to differentiating between regions within a country, which could also set a challenging precedent. Treating products from California differently than products from Texas—or Alberta differently from other Canadian provinces—may be interpreted as intruding in domestic policy. In this context, concerns about extraterritoriality may arise, which generally refers to situations where a jurisdiction seeks to regulate conduct occurring outside its borders (Parrish 2008). While CBAM functions as a de facto market access measure—conditioning access to the EU market on payment for carbon content—rather than an attempt to regulate foreign production, its differing impacts across regions within a country may be politically contentious.

However, the decision not to recognize subnational carbon pricing also creates incentives and has political consequences. In some cases, ignoring subnational policies may distort incentives more severely. From a climate policy perspective, approaches that recognize carbon costs can reward lower-carbon production for either producers or countries and encourage the adoption of carbon pricing policies.

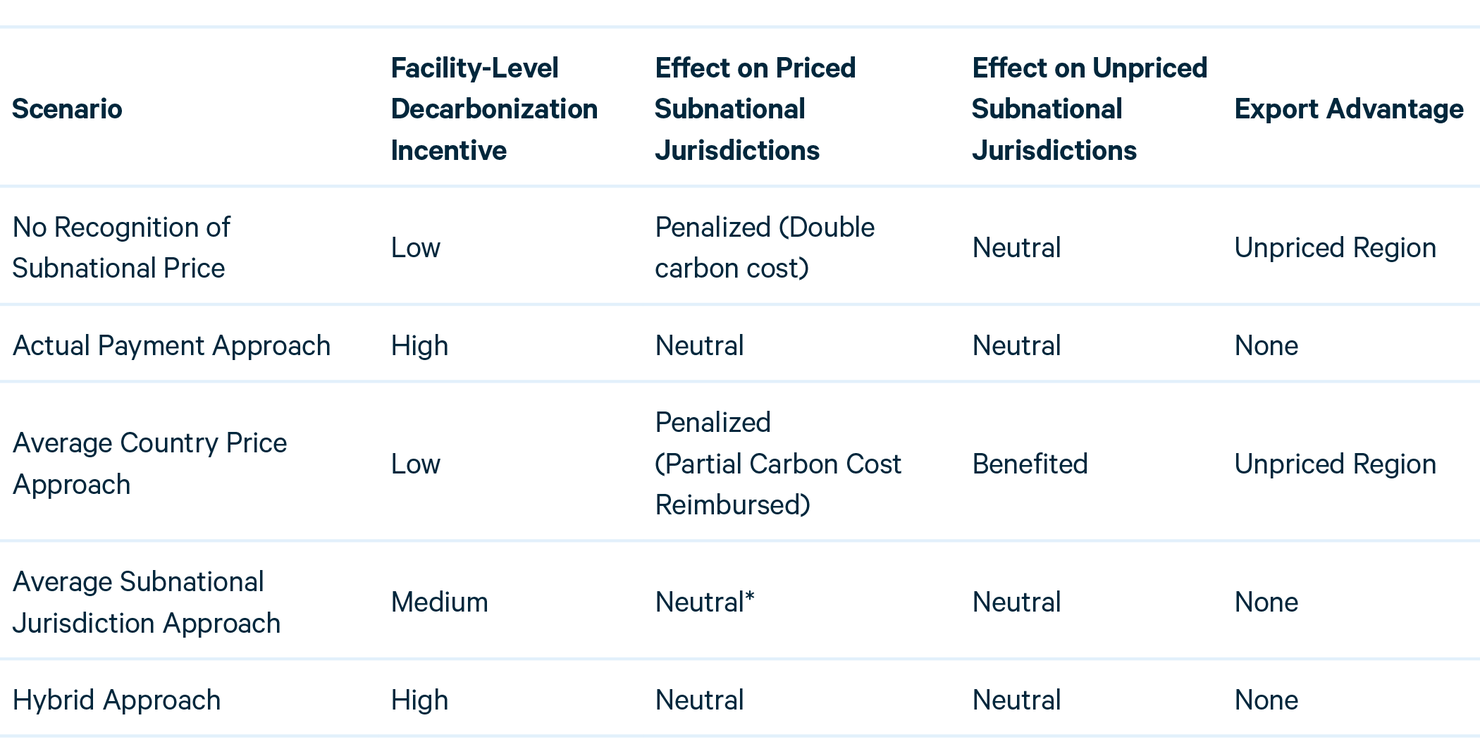

The incentive effects can be illustrated across five primary scenarios: (1) no recognition of subnational carbon pricing, (2) actual payment approach, (3) average-price approach of the national jurisdiction, (4) average-price approach of the subnational jurisdiction, and (5) a hybrid approach in which producers may use a default average or provide actual price data.

3.1. No Recognition of Subnational Carbon Pricing

If a CBAM does not recognize subnational carbon pricing, producers in carbon-priced regions would face a double burden: they would pay a carbon price domestically and again under CBAM. Producers in unpriced regions would face only the CBAM.

This approach penalizes early adopters of carbon pricing and weakens (or even disincentivizes) subnational jurisdictions from implementing carbon pricing.

3.2. Actual Payment Approach

Under the actual payment approach, facilities receive credit for the carbon costs they demonstrably pay. This preserves installation-level decarbonization incentives and avoids penalizing jurisdictions that have adopted carbon pricing.

However, this method increases reporting burdens and raises concerns about reshuffling within facilities. Firms could strategically allocate freely allocated allowances to domestic sales while assigning purchased allowances to exports. Certain safeguards would be necessary to prevent strategic allocation.

Despite these challenges, the actual payment approach most closely aligns crediting with carbon costs actually borne by producers.

3.3. Average National Price Approach

Under an average national price approach, carbon costs are calculated across the entire country and applied uniformly. In this scenario, producers in carbon-priced jurisdictions receive only partial credit for the carbon costs they paid, while producers in unpriced regions benefit from the reduction generated by priced regions. This approach also risks disincentivizing subnational carbon pricing.

Importantly, this approach may interfere more with domestic political dynamics. By pooling priced and unpriced regions together, it effectively penalizes jurisdictions that have adopted climate policy while implicitly rewarding those that have not.

3.4. Average Subnational Jurisdiction Approach

A subnational average approach differentiates across regions but treats all facilities within a region uniformly.

Compared to the actual payment approach, this weakens facility-level incentives. High-emitting and low-emitting installations within the same jurisdiction would receive identical treatment, creating potential free-riding risks. However, this approach would strengthen incentives for subnational carbon pricing.

3.5. Hybrid Approach

A hybrid approach—using an average price as a default while allowing facilities to demonstrate actual payments—offers a potential middle ground.

This would preserve facility-level decarbonization incentives where reliable data is available. It reduces the risk of penalizing subnational climate leadership while maintaining a manageable verification framework for importing authorities.

Table 1. Incentive Effects Across Scenarios

*Free-riding risk for carbon-intensive facilities within the priced subnational region.

4. An Example: Accounting for California’s Carbon Price

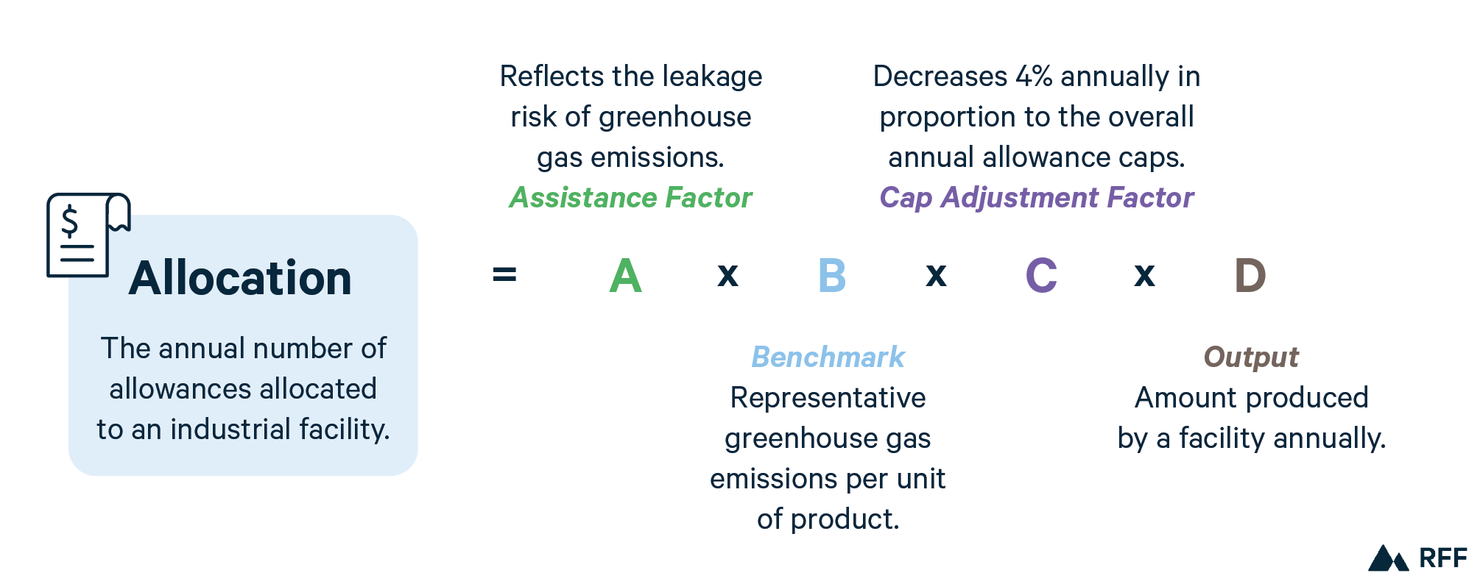

As a major cap-and-trade (CaT) system, California is a useful example to illustrate how subnational policies could be accounted for. The California CaT operates under nontrivial prices, at approximately $28 dollars in quarter four of 2025 (California Air Resources Board n.d.). While industries mostly receive free allocations, the California Air Resources Board has been increasing the stringency of the program by lowering the cap adjustment factor. Within California, most allowance allocations to industrial facilities are calculated through product-based benchmarking. The formula below gives a simplified look at how allocations in California are calculated.

Free allocation is determined by the facility’s level of output, the sector-specific benchmark, and the assistance factor. As a result, facilities operating at or below the benchmark can receive allowances covering most or all of their emissions, while facilities with higher emissions intensity must purchase additional allowances. Several factors can reduce the number of free allowances a facility receives, including operating above the benchmark, a decline in the cap adjustment factor, or changes to assistance factors over time. Additional compliance strategies—such as the use of banked allowances or offsets—can further reduce the number of allowances a facility needs to purchase.

California benchmarks are generally set at 90 percent of the sector’s production-weighted average emissions intensity over a historical baseline period. In cases where this would imply a benchmark more stringent than the emissions intensity of the most efficient facility in California, the benchmark is instead set equal to that best-performing facility. This differs from the EU Emissions Trading System, where benchmarks are based on the average emissions intensity of the top 10 percent most efficient installations, making EU benchmarks more stringent. Consequently, California’s benchmarking approach generally results in higher levels of free allocation and lower effective carbon costs for covered facilities, and therefore less crediting.

Figure 1. Allowance Allocation Formula for California’s Cap-and-Trade System

Source: California Air Resources Board (n.d.).

The distinction between nominal carbon prices and effective carbon costs is central to how California’s system would be credited. While a carbon price exists, the share of emissions actually subject to the price depends heavily on allocation design. Different emissions trading systems are bound to use different approaches than the EU. Some accounting for free allocations is necessary; however, rather than attempting to harmonize policy designs, policymakers face a trade-off between accuracy, administrative feasibility, and incentives when determining how to measure carbon costs.

Under the actual payment method, the European Union would require the declarant to provide documentation for any carbon price paid per unit of product. Using invoice documentation, the declarant must convert installation-level carbon costs to product-level costs to determine the overall carbon cost per unit of product. It would then be relatively straightforward to calculate the reduction in necessary CBAM certificates. In situations where all allowances were freely allocated, there would be no reduction in payment obligation. Using this method the European Union would not need to explicitly consider California separately from the United States and would not need to explicitly understand individual national and subnational pricing schemes and compensation mechanisms. All reporting burdens would be placed on the declarant, who has an incentive to provide the documentation of purchased allowances.

This method could result in an incentive for declarants to claim free allocations for domestically sold products and purchased allowances for exported products. This could be mitigated by calculating average product-level carbon costs from installation-level data. However, doing so would introduce significant complexity, particularly for multi-product facilities or supply chains spanning multiple facilities.

Under the average-price method, the economy-wide or sector-specific average carbon price would be calculated across the jurisdiction. Average product-specific rebates or free allowances would then be deducted from the overall price. If the average-price approach was based off the entire United States, then EU authorities would need to calculate the weighted average of all carbon prices across the United States—which would be very low. While Clausing and Wolfram (2023) estimate a weighted average carbon price of around $25 per ton, this reflects prices in covered jurisdictions rather than economy-wide exposure. Roy and Dolphin (2024) estimate an emissions-weighted average closer to $3 per ton. Restricting only on industrial products covered by CBAM—where explicit carbon pricing is more limited—would push the effective price closer to zero. Any CBAM reductions would likely approach zero in this case, as facilities covered by a carbon pricing scheme would be relatively low and likely receive large amounts of free allowances. Using this methodology, a product exported from California or Pennsylvania would be subject to the same reductions (or lack thereof).

However, an average-price approach could also be applied at the system level, considering the average carbon price within the state. In this situation a product exported from California would be subject to the average price in California less average free allocations. This would raise the deduction to the effective industrial carbon price in California, which is likely non-zero. Therefore, California and Pennsylvania products would be treated differently, while producers in low-emission and high-emission facilities within California would be treated the same.

A hybrid approach could also be taken, in which the average-price method is used as a default, however facilities are able to use the actual payment method if they are able to provide evidence. The hybrid approach could perhaps enhance interoperability, as it would allow more flexibility for different situations while relieving administrative efforts for regions that lack data capabilities.

The inclusion of downstream goods in CBAM coverage would add an additional layer of complexity for subnational carbon price crediting by extending the need to track carbon costs along fragmented supply chains. For example, California-produced steel subject to a carbon price could be exported to a neighboring state without carbon pricing and incorporated into a downstream product, such as a vehicle component, covered by CBAM. Crediting in this context would require documentation linking the carbon price paid on upstream inputs to the downstream product across jurisdictions.

California illustrates that carbon pricing can occur at the subnational level and can meaningfully affect production decisions. Failing to recognize these policies under CBAM would risk penalizing jurisdictions that have already implemented climate policy. However, recognizing subnational pricing raises nontrivial challenges for how carbon costs are measured and credited, which can be extended to all carbon pricing programs.

5. Looking Ahead: Recognizing Carbon Prices in a Diverse and Uneven Policy Landscape

CBAMs are typically designed as a leakage-prevention mechanism to equalize domestic carbon prices on the import market. In doing so, they must translate facility-level policies into product-level costs while avoiding (the perception of) discrimination between countries. Maintaining product-based logic requires careful consideration of how carbon costs are recognized.

If carbon-price jurisdictions receive little or no credit for the costs they impose domestically, CBAM may influence domestic policy dynamics within exporting countries in unintended ways. As carbon border adjustments expand beyond the European Union, the methodological choices adopted today may shape emerging norms. Approaches based on national averages emphasize jurisdiction-wide policy, while product- or installation-level approaches more directly incentivize changes in production methods, over which firms have greater control. Approaches that recognize carbon payments at the product or installation level better preserve decarbonization incentives, whereas approaches that prioritize protection of domestic industry may place less emphasis on such recognition.

Each method involves trade-offs between administrative feasibility, incentives, and political sensitivities. Recognition of carbon prices already paid in general, and especially by subnational entities, is a design feature which will affect interoperability as well. International initiatives where countries meet to discuss and align carbon pricing policies, such as the Open Coalition and Integrated Forum, launched at COP30, may be suitable venues to further discuss this issue of subnational carbon pricing treatment.

Ideally, crediting would take an automatic, rules-based approach to the greatest extent possible. However, given the many unique dynamics of individual carbon pricing systems, some degree of negotiation (to agree on interpretation of certain rules) between countries may be inevitable. Therefore, it is ideal to have established rules and norms, which may need to be supplemented by bilateral agreements. Opening up negotiations to discretionary deals risks opening the door to accusations of preferential treatment while dampening spillover incentives.

Looking ahead, these trade-offs may become more pronounced as countries adopt different approaches to carbon pricing and border measures. For example, in the United States, federal carbon pricing may remain unachievable, while a growing number of states implement their own carbon pricing systems. At the same time, other jurisdictions—such as Australia, the United Kingdom, and Canada—may move forward with their own carbon border measures. In such a policy landscape, questions around how to recognize subnational carbon pricing and measure effective costs become increasingly relevant.